共和党はOne Big, Beautiful Bill (OBBB) を提出しました。野心的な7月4日の「締め切り」までに完了するとは思っていませんでしたが、トランプ大統領は独立記念日に法案に署名しました。彼は基本的に欲しいものをすべて手に入れた。

1月、共和党の税金と支出の野心の幅広い輪郭が注目されたばかりの頃、私はブルームバーグのスカーレット・フーとの通過の見通しについて話しました。私たちの会話をここで要約しました:

共和党が月曜日の朝にトライフェクタになるのは事実ですが、1つの大きな和解法案で税金、国境、強制送還、規制緩和を行うパッケージをフィニッシュラインを越えて取得することはまだ難しいかもしれません。民主党が独自のトライフェクタを持っていたときにバイデンが発見したように、法案を通過させるのに十分な議席を持つことは、十分な票を持つことと同じではありません(上院議員を考えてください。マンチン(D-WV)と上院議員。シネマ(D-AZ)。一握りの共和党員がトランプの議題の一部を阻止できるだろうか?もちろん。実際、すでに下院で不満が醸成されているという報告があります。しかし、私がスカーレットに言ったように、トランプ次期大統領が求めていたことのほとんどを彼らが通過さなければ、私は驚くだろう。

スカーレットは、共和党員が「現代金融理論の考えを受け入れ、赤字を賄うために必要なお金を印刷する」ことを想像できるかどうか尋ねました。セグメントの終わりに到達していることを知っていたので、政府金融の仕組みを踏む時間はありませんでした(すべての政府支出は、新しいお金の存在にキーストロークによってすでに資金提供されていることを説明するために)、しかし、MMTレンズをどのように適用してGOPの税金と支出の野心を評価することができるかを説明しました。

最近の一連のインタビューで、その点を詳しく説明する機会がありました。David SirotaとのThe Leverポッドキャスト、Meghna ChakrabartiとのNPRのOn Point、Romaine BostickとのBloombergのThe Closeです。MMTレンズを通してOBBBを見て、私は法案の「値札」に不安を少なくし、人間的、環境的、インフレの影響にもっと関心があると説明しました。これらの懸念事項のそれぞれについて少しお話しします。

人間の通行人

人の被害に関しては、この法案はアメリカで最も脆弱な人々に壊滅的な影響を与えるでしょう。2017年の減税と雇用法(TCJA)とは異なり、OBBBは、減税と逆的な減税と逆的な支出削減を組み合わせた、多かれ少なかれ直接的な税法案でした(ただし、上層部に有利な暴利を大きく傾けています)。支出削減は非常に大きいため、議会予算局(CBO)は、減税自体が低所得世帯にもたらしたであろう利益を消す以上のものに、支出削減が排除することを示しています。

全体として、OBBBは何百万人ものアメリカ人と企業に減税と新しい金融特典を提供し、メディケイドや食糧支援(SNAP)などのプログラムから何百万人もの同じ人々が受け取る支援を取り戻します。多くの専門家によると、これは米国史上最大の社会的セーフティネットの削減につながるだろう。それは低所得のアメリカ人を一回し、今後10年間で最悪の場合に終わるでしょう。メディケイドとアフォーダブルケア法の削減により、200万人のチップ労働者が健康保険を失うリスクがあります。

すべてが言われて完了すると、1700万人ものアメリカ人が健康保険の適用範囲を失う可能性があり、子供と家族は飢え、農村部の病院は閉鎖され(まともな給料の仕事も取り下げられ)、毎年51,000人以上の予防可能な死亡が見られる可能性があります。私がここで書いたように、OBBBは、すでに実質的な経済的安定を享受している人々にさらに多くの富を注ぎながら、所得分配の最下位の人々から資源を奪うひどい法律です。これは、民主党がしばらく強調してきたOBBBの特徴(バグではない)であり、有権者が来年の投票に向かうときに注目することを望んでいるものです。上院民主党院内総務のチャック・シューマーです。

私たちはあらゆる点で彼らの状態にいるつもりです。私たちは整理するつもりです。傷ついた人全員を組織化します。あなたはそれらの州で絶え間ない、絶え間ない戦いを見るでしょう、人々に起こったことを毎日思い出させます。そして、それは上院の民主党員になるでしょう。ひどく傷ついたのは、すべてのグループです。普通の人になるでしょう。先月、何人の人が行進したか見ましたね。この「大きくて醜い裏切り」に対するより多くの行進、より多くの抗議が行われるでしょう。

共和党は、彼らがここで脆弱であることを認めています。そのため、セーフネットへの最も厳しい削減の多くは2027/28まで拡大しない一方で、減税がすぐに当たるように法案を構成しました。トランプ大統領と彼の同盟国は、家族が痛みを感じる前に、法律の特典を感じることを望んでいます。(法案の潜在的なインフレリスクについて私が考える方法に不可欠であるため、これについては戻ってきます。)それはまた、数千万人のMAGA有権者を含む有権者を説得することになると、民主党員が彼らを狼に投げつけたことで罰せられるべきだということになることを意味します。

環境被害

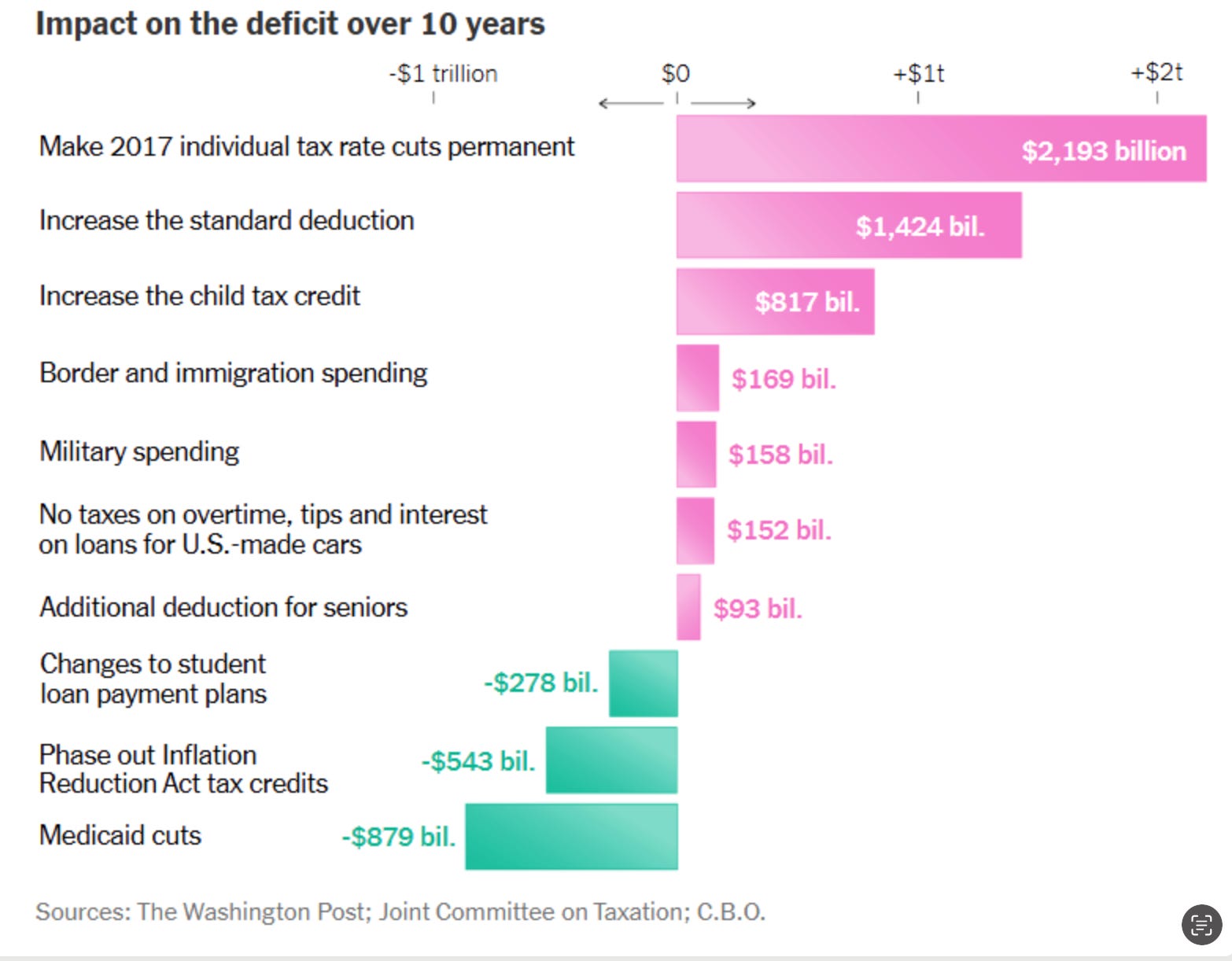

環境に関しては、OBBBは、企業やアメリカの消費者によるクリーンエネルギーの開発と採用を促進することを目的とした5,430億ドル相当の税制優遇措置を廃止します。気候専門家は、それが「何千ものクリーンエネルギーの雇用を破壊し、私たち全員を気候災害からより大きなリスクにさらす」と警告しています。

インフレ削減法(IRA)の大幅なロールバックにより、シエラクラブの気候政策ディレクターであるパトリック・ドラップは、OBBBを「歴史上最も反環境法案」と呼びました。これらの減税措置を撤廃することは、エネルギー需要が歴史的な速度で増加している時に、比較的迅速に追加できる発電である風力発電と太陽光発電を送電網に持ち込む方がより費用がかかることを意味します。これは、ロールバックされるIRA規定の優れた要約です。一方、Dana Drugmandは、この法案は「冶金石炭の生産に税額控除を延長し、メタン排出を抑制することを目的としたプログラムを麻痺させ、石油回収の強化を含む炭素回収および貯蔵プロジェクトの税額控除レベルを引き上げます。これは、石油生産を刺激するために二酸化炭素を使用した掘削の一種です。」

私はOBBBの環境への負担について何日も書くことができますが、気候分野の専門家の仕事を参照して要約するだけです。ここ、ここ、ここ、ここ、ここでもっと読むことができます。ご想像のとおり、人間の健康やインフレなどの他の懸念分野に波及する環境被害に関連する外部性があります。

インフレリスク

OBBBが国内生産と雇用をどの程度まで引き上げるかについては、さまざまな意見があり、いくつかの激しい論争があります。法案の擁護者は、近い将来に実質GDP成長率を4.9%に押し上げる、本物のトリクルダウンの奇跡を目撃しようとしていると信じさせるだろう。それはホワイトハウス経済顧問評議会(CEA)が宣伝していることです。

批評家はCEAのバラ色の見通しを嘲笑し、ホワイトハウスのエコノミストが、より信頼できる予測者によって予測されているものとは似ていない「ファンタジー」の仮定に基づいて予測していると非難しています。

トランプ政権がこれらの目を見張るような成長予測を宣伝している理由の1つは、共和党が「大規模な」法案の予算効果、つまり債務と赤字について圧力をかけられていることです。爆発的な成長を想定することで、彼らは自分たちがやっていることは財政的に無責任ではないという考えで金融市場(および有権者)を売りたいと考えています。

さまざまなインタビューで述べてきたように、私は議会予算局(CBO)、イェール予算研究所(YBL)、ペンワートン予算モデル(PWBM)、または責任ある連邦予算センター(CRFB)がOBBBの予算効果について言わなければならないことに神経を抱いていません。私はMMTレンズを通して物事を見るので、税金と支出の請求書の「財政コスト」は、私が本当に気にしていることについて多くの洞察を与えてくれません。私が最も懸念しているのは、法案の人間的、分配的、環境的、そしてインフレ的な影響です。

私が何十年も主張してきた点は、インフレリスクに関しては、議会が支出を「支払っている」か、赤字を増やしているかを知るだけでは不十分だということです。その理由は、赤字は中立であるが、インフレ率が高く、したがって財政的に無責任である税金と支出法案をまとめるのはかなり簡単だからです。例えば、所得分配の上位1%の人だけに増税することで、寛大なユニバーサルベーシックインカム(UBI)を「支払いました」。それは、ほぼすべてのアメリカ人の支出をパンチアップし、トップの需要を抑制するために比較的ほとんど何もしないでしょう。逆に、インフレ率を下げながら財政赤字を大幅に増加させる法案を起草することができます。たとえば、メディケア・フォー・オールなどの単一支払者医療などです。 GDPに占める医療費(公共部門+民間部門)の合計は、約18%から15%に低下する可能性があります(メディケア・フォー・オールのどのバージョンを検討しているかによって異なります)、実質的なリソース(労働力を含む)を解放します。したがって、赤字の一般的な増加は必然的により高いインフレにつながるか、議会はすべての赤字を中立に保つことでインフレを回避できると仮定するのは間違いです。

MMTの観点から、セクターの金融バランスを理解することは、すべての政府赤字の反対側に、経済の他の部分に蓄積されたマッチング(金融)余剰があることを理解することを意味します。誰がそれらの支払いを受け取るか、そしてそのお金が商業の静脈に入るかどうか、そしてどのように、つまり既存の商品やサービスを追いかけるか、新しい投資に拍車をかけるかは、赤字の良性の増加(2009年のアメリカ救済復興法または2017年の減税雇用法に続いてあったように)と、インフレを混乱させるものとの違いを綴ることができます。

上記の見出しマクロ予測(CBO、PWBM、YBL、CFRFB)のどれも、OBBBが破滅的なインフレにつながると予測していないことは注目に値します。部分的には、彼らはパッケージを短期的には控えめに拡張的であると見なしているからです。税金面で起こることのほとんどは、2017年の減税の延長にすぎないので、その面で心配する新しい財政衝動はなく、多くの新しいもの(チップ/残業/自動車ローンの利息などに対する税金なし)は数年後に失効します。新しい税金と防衛と移民への短期的な支出の増加を組み合わせると、すべてのヘッドラインモデルは控えめなインフレ圧力を予測し、FRBは金利を上げることで対抗します。金利が上昇するにつれて、すべてのモデルは、合理的に短期間でインフレ率をFRBの目標2%に押し下げるのに十分な民間部門の支出が追い出されることを前提としています。

したがって、これらすべてのモデルによると、OBBBの問題は、FRBが積極的に金融政策を引き締める必要があるほど多くの財政刺激策を提供することではありません。インフレを抑えるには、金利のわずかな上昇が必要です。CBO(および他の人々)によると、問題は、2017年の減税が期限切れを許され、時間の経過とともに財政赤字が縮小したベースラインケースと比較して、経済のパフォーマンスが悪化するということです。これらすべての物語において、赤字が原因であり、インフレではなく、成長が遅い経済が罰です。

ホワイトハウスはこれらすべてに異議を唱えている。トランプ大統領は、今後数か月、数年で、金利が高くなるのではなく、下がることを望んでおり、期待しています。彼の政権は、OBBBの結果として、より急速な経済成長を見ています。そして、トランプチームは、製造業の拡張と人工知能(AI)の進歩が生産性の奇跡をもたらすにつれて、インフレは上昇ではなく減少する傾向にあると考えています。

より速い成長。インフレ率を下げる。より低い金利。

ケビン・ハセット(ホワイトハウス国家経済評議会のディレクター)、スティーブン・ミラン(ホワイトハウス経済諮問委員会の議長)、スコット・ベセント(米国)財務長官)はすべて有望です。7月7日のCNBCのインタビューで、ベッセント長官は「インフレのない方法で経済成長を遂げるつもりだ」と述べた。1週間前の共同論説で、ハセットとミランは次のように書いています。

提起されたもう一つの議論は、この法案が成長が離陸するにつれてインフレを上昇させるということです。もちろん、この見解を持つ人々は、米国の生産を増やす工場支出ブームが供給を増やすことによってインフレを低下させるという事実を説明していません。バイデン政権は政府支出でインフレに火をつけ、供給を妨げるために急上昇する規制を使用した。今日の提案された政策の効果を見るには、低で安定したインフレを伴う2017-19年の成長の加速に目を向けてください。

新しい投資を刺激するように設計された税制優遇措置から、ピカピカの新しい工場自体に直接ジャンプできればいいのですが、それは物事のやり方ではありません。新しい製造能力の構築が価格を押し下げる前に、これらすべての新しい工場を建設する必要があります。そして、それには労働力(必要なスキル)、資本設備、木材、鉄鋼、コンクリート、銅などが必要です。主要なインプットに対する高い(そして上昇する)関税、大量強制送還による労働力の縮小、そして医療、エネルギー、その他のコストを大幅に押し上げる予算法案で、これらすべてが非インフレ的な方法でどのように起こることになっているのでしょうか?

「解放の日」のずっと前に、ベッセント長官は関税の使用を擁護し、「関税はインフレにはならない。なぜなら、ある物の価格が上がると、人々にもっとお金を与えない限り、他のものに費やすお金が少なくなるため、インフレはない」と主張した。

さて、共和党は、ほぼ全員により多くのお金を与える法案を可決したばかりです(同時に、より高いエネルギー、医療、およびインフレに直接供給するその他のコストの段階を設定します)。それで、私は心配ですか?間違いない。

What Worries Me About the 'Big Beautiful Bill' Isn't the Price Tag. It's Everything Else.

Republicans have delivered on the One Big, Beautiful Bill (OBBB). I didn't expect it to get it done by the aspirational 4th of July "deadline," but President Trump signed the bill into law on Independence Day. He basically got everything he wanted.

Back in January, when the broad contours of the GOP's tax and spending ambitions were just coming into focus, I talked about the prospects for its passage with Bloomberg's Scarlet Fu. I summarized our conversation here:

While it's true that republicans will have a trifecta come Monday morning, it could still prove difficult to get a package that does tax, border, deportation, and deregulation in one big reconciliation bill across the finish line. As Biden discovered when democrats had their own trifecta, having enough seats to pass legislation isn't the same thing as having enough votes (think Sen. Manchin (D-WV) and Sen. Sinema (D-AZ). Could a handful of republicans thwart parts of Trump's agenda? Sure. In fact, there are already reports of frustration brewing in the House. But as I told Scarlet, I would be surprised if they don't end up passing something that does most of what President-elect Trump has called for.

Scarlet asked whether I could envision republicans "embracing the idea of Modern Monetary Theory and just printing the money needed to finance the deficits." I knew we were reaching the end of the segment, so there was no time to walk through the mechanics of government finance (to explain that all government spending is already financed by keystroking new money into existence), but I did explain how the MMT lens could be applied to evaluate the GOP's tax and spending ambitions.

I had a chance to elaborate on that point in a series of recent interviews: The Lever podcast with David Sirota, NPR's On Point with Meghna Chakrabarti, and Bloomberg's The Close with Romaine Bostick. Looking at the OBBB through the MMT lens, I explained that I was less unnerved by the bill's "price tag" and more concerned with its human, environmental, and inflationary impacts. Let me say a few words about each of these concerns.

The Human Toll

When it comes to the human toll, the bill will have devastating effects on the most vulnerable people in America. Unlike the 2017 Tax Cuts and Jobs Act (TCJA), which was more-or-less a straight up tax bill that sprinkled relief across the entire income distribution (though tilting the windfall heavily in favor of those at the top), the OBBB combines regressive tax cuts with regressive spending cuts. The spending cuts are so large that the Congressional Budget Office (CBO) has shown that they will more than erase the benefits that the tax cuts themselves would have delivered to low-income households.

Taken as a whole, the OBBB provides tax relief and new financial perks for millions of Americans and businesses while clawing back support that millions of these same people receive from programs like Medicaid and food assistance (SNAP). According to many experts, this will result in the largest cuts to the social safety net in US history. It will clobber low-income Americans, who will end up— on balance—worse off in the coming decade. Two million tipped workers are among those at risk of losing health coverage because of the cuts to Medicaid and the Affordable Care Act.

When all is said and done, as many as 17 million Americans could lose their health insurance coverage, kids and families will go hungry, hospitals in rural communities will shutter (taking decent-paying jobs down with them), and we could see more than 51,000 preventable deaths each year. As I wrote here, the OBBB is an egregious piece of legislation that strips resources from those at the bottom of the income distribution while showering even more wealth onto people who already enjoy substantial economic security. That's a feature (not a bug) of the OBBB that democrats have been highlighting for some time and something they're hoping voters will focus on when they head to the polls next year. Here's Senate Democratic Leader Chuck Schumer:

We're going to be in their states in every way. We are going to organize. We are going to have all the people who are hurt organized. You're going to see a constant, constant battle in those states, reminding people day in and day out of what happened. And that's going to be Democrats in the Senate. It's going to be all of the groups who were hurt so badly. It's going to be just average folks. You saw how many people marched last month. There'll be many more marches, many more protests against this "Big, Ugly Betrayal."

Republicans admit they're vulnerable here, which is why they've structured the bill so that the tax cuts hit right away while many of the harshest cuts to the safety net don't ramp until 2027/28. President Trump and his allies want families to feel the perks of the legislation before they feel its pain. (I'll come back to this as it's crucial to the way I think about the bill's potential inflation risk.) It also means that democrats will have their work cut out for them when it comes to persuading voters, including tens of millions of MAGA voters, that republicans should be punished for throwing them to the wolves.

The Environmental Damage

When it comes to the environment, the OBBB eliminates $543 billion worth of tax incentives aimed at boosting the development and adoption of clean energy by businesses and American consumers. Climate experts warn that it "destroys thousands of clean energy jobs, and puts us all at greater risk from climate disasters."

Because of the substantial rollback in the Inflation Reduction Act (IRA), Patrick Drupp, director of climate policy for the Sierra Club., has dubbed the OBBB "the most anti-environment bill in history." Removing those tax breaks means that it will be more expensive to bring wind and solar—generation that can be added relatively quickly—onto the grid at a time when energy demand is rising at a historic rate. Here's an excellent summary of the IRA provisions that get rolled back. Meanwhile, Dana Drugmand writes that the bill "extends a tax credit to production of metallurgical coal, ….cripples a program intended to crack down on methane emissions, … and raises the tax credit level for carbon capture and storage projects that involve enhanced oil recovery—a type of drilling using carbon dioxide to stimulate oil production."

I could write for days about the OBBB's environmental toll, but I would just be referencing and summarizing the work of experts in the climate space. You can read more here here here here here and here. As you might imagine, there are externalities associated with the environmental harms that spill over into other areas of concern, like human health and inflation.

The Inflation Risk

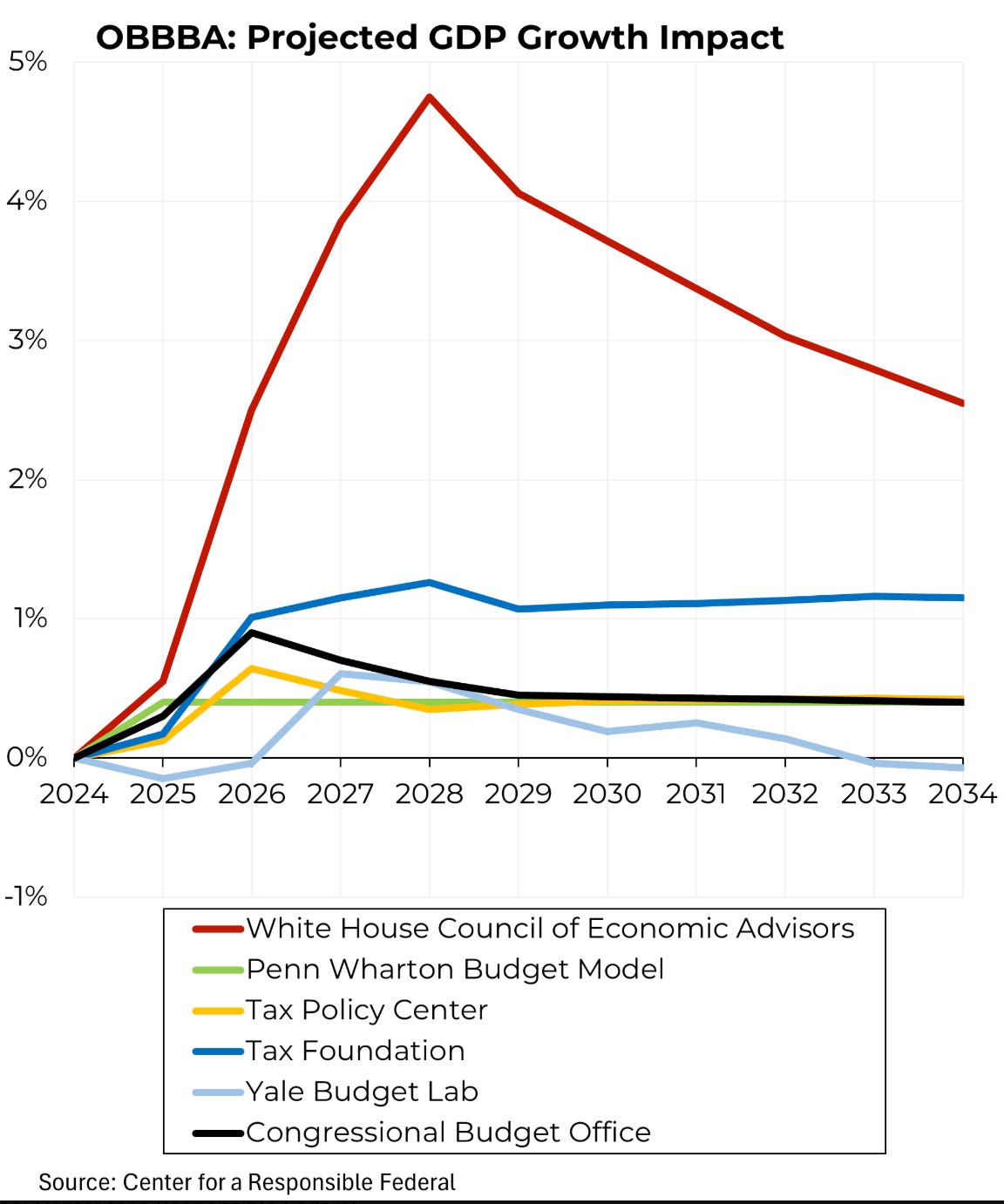

There are various opinions—and some heated disputes—about the extent to which the OBBB will juice domestic production and employment. Champions of the bill would have us believe that we're about to witness a bonafide, trickle-down miracle that will push real GDP growth as high as 4.9% in the near term. That's what the White House Council of Economic Advisors (CEA) is touting.

Critics are mocking the CEA's rosy outlook, accusing White House economists of basing their projections on "fantasy" assumptions that look nothing like what's being predicted by more credible forecasters.

One of the reasons the Trump administration is touting these eye-popping growth projections is that republicans are being pressed on the budgetary effects—i.e. debt and deficit—of their "massive" bill. By assuming explosive growth, they hope to sell financial markets (and voters) on the notion that what they're doing isn't fiscally irresponsible.

As I've been saying in various interviews, I'm not unnerved by what the Congressional Budget Office (CBO), the Yale Budget Lab (YBL), the Penn Wharton Budget Model (PWBM), or the Center for a Responsible Federal Budget (CRFB) have to say about the budgetary effects of the OBBB. I look at things through an MMT lens, so the "fiscal cost" of the tax and spending bill doesn't give me a lot of insight into the things I really care about. What I'm most concerned about are the bill's human, distributional, environmental, and inflationary impacts.

A point I have been making for decades is that when it comes to inflation risk, it's not enough to know whether Congress is "paying for" its spending vs. adding to the deficit. The reason is that it would be pretty easy to assemble a tax and spending bill that is deficit neutral but highly inflationary and therefore fiscally irresponsible—e.g. a generous Universal Basic Income (UBI) "paid for" by raising taxes only on those in the top 1% of the income distribution. That would punch up spending by almost every American while doing relatively little to curb demand at the very top. Conversely, I could draft legislation that substantially increases the fiscal deficit while dragging inflation lower—e.g. single-payer health care such as Medicare for All. Total (public + private sector) spending on healthcare as a share of GDP might fall from around 18% to something like 15% (depending on which version of Medicare for All we're considering), freeing up substantial real resources (including labor). Hence, it would be a mistake to assume that any generic increase in the deficit will necessarily lead to higher inflation or that Congress can avoid inflation by keeping everything deficit neutral.

From an MMT perspective, understanding the sector financial balances means understanding that on the other side of every government deficit lies a matching (financial) surplus that accumulates in some other part of the economy. Who receives those payments, and whether and how that money goes on to enter the veins of commerce—chasing after existing goods and services or spurring new investment—can spell the difference between a benign increase in the deficit (like we had following the 2009 American Rescue and Recovery Act or the 2017 Tax Cuts and Jobs Act) and one that makes a mess of inflation.

It's worth noting that none of the headline macro forecasts referenced above (CBO, PWBM, YBL, CFRFB) predict that the OBBB will lead to ruinous inflation. In part, that's because they view the package as only modestly expansionary in the short-run. Most of what happens on the tax side is just an extension of the 2017 tax cuts, so there's no new fiscal impulse to worry about on that front, and a lot of the new stuff (no tax on tips/overtime/auto loan interest/etc.) expires after a few years. When you couple the new tax stuff with higher near-term spending on defense and immigration, all of the headline models project modest inflationary pressures, which the Fed counters by raising interest rates. As interest rates move higher, all of the models assume there will be enough crowding out of private sector spending to push inflation down to the Fed's 2 percent target in a reasonably short period of time.

So the problem with the OBBB, according to all of these models, isn't that it provides so much fiscal stimulus that it requires the Fed to aggressively tighten monetary policy. It takes only a modest rise in interest rates to hold inflation in check. The problem, according to CBO (and the others), is that you end up with a worse performing economy relative to a baseline case where the 2017 tax cuts were allowed to expire, shrinking the fiscal deficit over time. In all of these stories, the deficit is the culprit, and a slower-growing—not inflationary—economy is the punishment.

The White House disputes all of this. President Trump wants—and expects—interest rates to be lower, not higher, in the coming months and years. His administration sees more rapid, not slower, economic growth as a result of the OBBB. And the Trump team believes that inflation will trend down, not up, as manufacturing capacity expands and advances in Artificial Intelligence (AI) deliver a productivity miracle.

Faster growth. Lower inflation. Lower interest rates.

That's what Kevin Hassett (director of the White House National Economic Council), Stephen Miran (chairman of the White House Council of Economic Advisers), and Scott Bessent (U.S. Treasury Secretary) are all promising. In July 7 interview on CNBC, Secretary Bessent said, "We're going to have economic growth in a non-inflationary manner." In a joint op-ed a week earlier, Hasset and Miran wrote:

Another argument raised is that the bill will cause inflation to pick up as growth takes off. Those with this view, of course, fail to account for the fact that a factory spending boom that increases U.S. production drives down inflation by increasing supply. The Biden administration threw fire on inflation with government spending and used skyrocketing regulations to impede supply. To see the effect of today's proposed policies, look no further than the 2017-19 acceleration in growth that was accompanied by low, stable inflation.

It would be nice if we could jump directly from the tax incentives that are designed to spur new investment to the shiny new factories themselves, but that's not how things work. Before a build-up in new manufacturing capacity can help drive down prices, all of those new factories have to be built. And that requires labor (with the requisite skills), capital equipment, lumber, steel, concrete, copper, etc. How is all of this supposed to happen in a non-inflationary way with high (and rising) tariffs on key inputs, a shrinking labor force via mass deportation, and a budget bill that will significantly drive up health care, energy, and other costs?

Long before "Liberation Day," Secretary Bessent defended the use of tariffs, arguing that "tariffs can't be inflationary because if the price of one thing goes up—unless you give people more money—then they have less money to spend on the other thing, so there is no inflation."

Well, republicans just passed a bill that gives pretty much everyone more money (while setting the stage for higher energy, health care, and other costs that feed directly into inflation). So am I worried? You bet.

0 件のコメント:

コメントを投稿