https://youtu.be/ev823MkrcQk?si=vBC6N1qEV2D0M2e4

ピムコ、日本の超長期債への見方変えず-魅力的な投資機会と評価

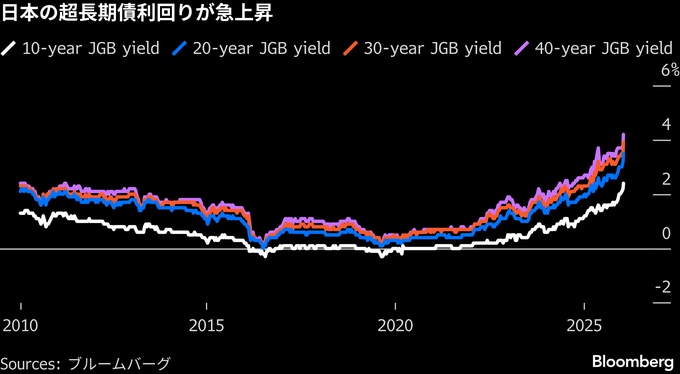

(ブルームバーグ):米パシフィック・インベストメント・マネジメント(PIMCO)は、先週の急落後も日本の30年物国債に対する見方を維持している。日本の債券市場に価値を見いだす投資家が増える中、同社もその一角に加わった。

ピムコは、足元の利回り水準が魅力的な投資機会を提供していると指摘。財政拡張への懸念を背景とした下落で約410億ドル(約6兆3300億円)が失われ、他国の債券市場にも売りが波及したが、利回りの上昇は金利低下時のキャピタルゲインをもたらす可能性があるほか、経済ショックや株式市場の変動、円の急騰に対するヘッジにもなるとした。

ピムコでアジア太平洋運用統括責任者を務める正直知哉氏はアウトルックリポートで、30年物国債などイールドカーブの長期ゾーンを選好する姿勢を維持していると説明。財政リスクへの懸念は残るものの、イールドカーブのスティープさや財務省が長めの債券発行を抑制するインセンティブがこのポジションを支えているとした。

こうした見解は、三井住友フィナンシャルグループやRBCブルーベイ・アセット・マネジメントなどの見方とも重なる。長年の金融緩和で利回りがほぼゼロ近辺に抑えられてきた後、日本の債券市場の振れに投資家が慣れてきたことを示唆している。2月8日投開票の総選挙を控え、為替介入を巡る思惑が円相場を揺らす中、落ち着いた局面を経て再び変動が大きくなることにトレーダーらは備えている。

世界最大級の債券運用会社であるピムコは、2025年半ばの混乱を伴う下落後にも、日本国債に関して同様に楽観的だった。当時、日本銀行によるさらなる量的引き締め(QT)の可能性は、日銀の買い入れが比較的少ないイールドカーブのロングエンドにかかる圧力を和らげるため、むしろ好材料になり得るとの見方を示していた。

ピムコは日銀が政策の正常化を段階的に進め、今後1年で政策金利を0.25-0.5ポイント引き上げ、1-1.25%とする可能性があると見込む。日銀は23日に政策金利を0.75%程度に据え置くと決めたが、植田和男総裁は必要に応じて債券市場のボラティリティーをならすためのオペを実施することがあり得ると付け加えた。

日銀は市場の安定を確保するため、極端な状況では臨時の国債買い入れオペで介入する可能性があると、正直氏は別の電子メールでの回答で記した。

ピムコは、指標となる10年債利回りが「おおむね現在の水準付近」で推移するとみており、26日時点では2.235%近辺だった。

グローバル投資家にとって、現在は為替ヘッジコストが追い風となっており、日本国債の相対的な魅力を高め、世界の同業資産と比べて追加的な利回りを提供していると、同チームは分析した。

ただ、利回りをこのレンジから外へ押し出しかねないリスクも複数ある。

円安や予想外のインフレ加速はより迅速、あるいはより大幅な政策金利引き上げを促す可能性があると、同チームは指摘。同時に、高市早苗政権の拡張的な財政スタンスは追加的な不確実性をもたらすものの、最終的には金融市場からの圧力が政策の行き過ぎの余地を抑えると見込んでいる。

原題:Pimco Stands by Japan Longer Bonds View After $41 Billion Rout(抜粋)

(情報を追加し更新します)

もっと読むにはこちら bloomberg.com/jp

©2026 Bloomberg L.P.