中銀のバランスシート・トリレンマ

というFRBノートをMostly Economicsが紹介している。原題は「The Central Bank Balance-Sheet Trilemma」で、著者はBurcu Duygan-Bump、R. Jay Kahn。

以下はMostly Economicsの引用部の孫引き。

In this note, we offer a framework for understanding the tradeoffs involved in determining the optimal size and behavior of a central bank's balance sheet. Specifically, we highlight that central banks face a "balance sheet trilemma," in that they can achieve only two of the following goals at once:

- a small balance sheet,

- low volatility of short-term rates, and

- limited market intervention.

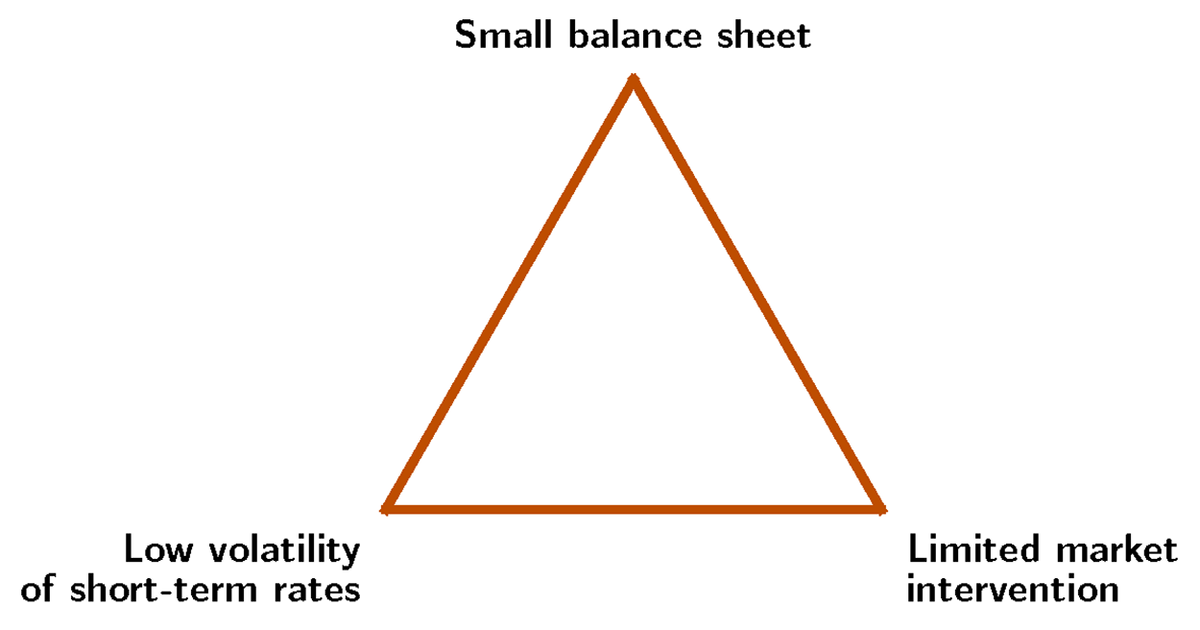

The underlying tension between these goals arises from the financial sector's demand for reserves and the frequency of sudden changes in liquidity demand and supply.3 Figure 1 displays these options visually.

Compromising on any of the three goals carries significant costs: 1) A large balance sheet increases the central bank's structural footprint in financial markets and could crowd out private sector credit intermediation. 2) High money-market volatility can dampen rate control, impeding the implementation of monetary policy and leading to unexpected funding stress and liquidity shortages. 3) Frequent market interventions expand the central bank's footprint through daily market operations, potentially impairing price discovery and market discipline. To be sure, the central bank can opt for an interior solution and tolerate some rate volatility (for instance, around calendar quarter-ends), some extra market operations, and a slightly larger balance sheet. But we hope the trilemma framework laid out here clarifies the tradeoffs central banks face.

(拙訳)

本ノートで我々は、中銀のバランスシートの最適な規模と行動を決定する際のトレードオフを理解するための枠組みを提示する。具体的には、中銀が「バランスシート・トリレンマ」に直面することを明らかにする。そのトリレンマにおいて中銀は以下の目標のうち2しか同時に達成できない。

- 小さなバランスシート

- 短期金利の低い変動性

- 限定的な市場介入

以上の目標の間に横たわる緊張は、金融部門の準備預金への需要と、流動性需給の突然の変化の発生頻度に起因する*1。図1はこの選択肢を視覚的に表現している。

Figure 1. The balance-sheet trilemma visualized

この3つの目標のいずれについても妥協は大きなコストを伴う。1) 大規模なバランスシートは金融市場への中銀の構造的な影響力を増し、民間部門の信用仲介をクラウドアウトしかねない。2) 金融市場の高ボラティリティは金利コントロールを弱め、金融政策の実施を阻害し、予期せぬ資金調達の混乱と流動性不足につながりかねない。3) 頻繁な市場介入は日々の市場操作を通じて中銀の影響を拡大し、価格発見と市場規律を損なう可能性がある。確かに中銀は中間的な解決策を採ることができ、ある程度(例えば毎四半期末)のボラティリティ、幾ばくかの余分な市場操作、少し大きめのバランスシートを許容することができる。とは言え、ここで提示するトリレンマの枠組みは中銀が直面するトレードオフを明確化するものと思う。

0 件のコメント:

コメントを投稿