| ||||||||||||||||||||||||

| ||||||||||||||||||||||||

劉尚希 / LIU Shangxi

中国 / China

財政部財政科学研究院院長

Yan Liang @YanLian31677392

news.caijingmobile.com/live/live/1131…

Live stream - Liu Shangxi, director of Chinese Academy of Fiscal Sciences speaking abt MMT. pic.twitter.com/jOwW9uM3R32022/06/14 11:56 https://x.com/yanlian31677392/status/1536543139598675970?s=61

财经号直播 | 现代货币理论与宏观经济政策走向

https://news.caijingmobile.com/live/live/1131

- UTSA

- CMF 2nd International

- Seminar on

- Macroeconomics

- MMT and Macroeconomic Policy Outlook

中国财政科学研究院院长刘尚希提出了四点看法。第一,财政是金融的基础,也是资本市场的基础。具体来说,国债和国债收益率曲线就是资本市场的基础设施,而中国国债收益率曲线的基础设施还需要进一步完善。第二,以支定收是现代预算的基本思维和程序。财政收支的运行过程已经嵌入到了央行货币发行和收回的过程,财政支出的过程就是货币发行的过程,征税的过程就是货币收回的过程,两者是紧密契合的。而且从政府承担公共责任、化解公共风险角度讲,政府规模是在扩大的。第三,赤字是一种常态。一方面,政府在面对有效需求不足时需要通过赤字扩大需求,赤字成为政府的政策工具。另一方面,现在的赤字越来越多地成为提供金融工具的渠道和途径,以发行国债的方式提供无风险的金融资产,为资本市场定价提供基准。第四,赤字是否导致通货膨胀是不确定的。在赤字规模与通胀的关系中,资源约束是一个条件,此外还有一个重要的条件就是宏观不确定性和风险防控的问题。

财经号直播 | 现代货币理论与宏观经济政策走向 劉尚希 LIU Shangxi

直播嘉宾:

毛振华 中国人民大学经济研究所联席所长、教授、中国宏观经济论坛(CMF)联席主席,中诚信集团董事长

刘元春 上海财经大学校长,中国人民大学原副校长、中国宏观经济论坛(CMF)联合创始人

刘尚希 中国财政科学研究院院长

邵 宇 东方证券首席经济学家

杨瑞龙 中国人民大学一级教授、经济研究所联席所长、中国宏观经济论坛(CMF)联席主席

Yan Liang 美国制度思想学会主席,威拉姆特大学经济学教授、Peter C. and Bonnie S. Kremer主席、国际研究主任

Yeva Nersisyan 富兰克林与马歇尔学院经济学副教授,利维经济研究院研究员

https://www.bloomberg.com/news/articles/2022-04-21/modern-monetary-theory-wins-new-fans-in-china-as-growth-tumbles

China’s Economists Are Getting Into Modern Monetary Theory

MMT in focus as fiscal stimulus to become mainstay this year China can consider U.S.-style QE, former PBOC adviser says

Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

Modern Monetary Theory can inspire China to make sure central bank easing supports government spending, several prominent economists said, as Beijing turns to fiscal policy to boost economic growth.

中国のエコノミストが現代通貨理論に傾倒 - Bloomberg

https://www.bloomberg.com/news/articles/2022-04-21/modern-monetary-theory-wins-new-fans-in-china-as-growth-tumbles

中国のエコノミストが現代金融理論に傾倒

中国、財政出動が主軸になる中、MMTに注目 米国型QEも検討可能、元中央銀行顧問が指摘

2022年4月22日 6:00 JST

新経済日報のニュースレターを購読する、@economicsをフォローする、ポッドキャストを購読する。

北京が経済成長を促進するために財政政策に目を向ける中、現代金融理論は、中央銀行の緩和が政府支出を確実に支えるよう中国を鼓舞することができると、複数の著名なエコノミストが語った。

贾根良:MMT及其对中国宏观经济政策制定的重要意义(ジア・ゲンリャン: MMTの重要性と中国の政策決定におけるMMT)Jia Genliang

2022/02/16 #159 Examining China with an MMT Lens with Yan Liang

| ||||||||||||||||||||||||

劉尚希. 1. Page 2. 一、中国のマクロ経済情勢の短期分析.. 1.足元の経済成長率は依然低下傾向.. 2015年第1四半期~2016年第1四半期のGDP成長率(四半期ベース ...

劉尚希先生是中國財政科學研究院黨委書記兼院長,經濟學博士,研究員、博士生導師。第十三屆全國政協委員,國務院政府特殊津貼專家、國家「百千萬人才工程 ...

刘尚希,经济学博士,研究员、博士生导师,中国财政科学研究院党委书记、院长,高端智库首席专家,国务院政府特殊津贴专家,国家文化名家暨“四个一批”人才。

2023/11/3 -Bank of China Securities主任エコノミストのGuan Tao氏はCMGに対し、中国は将来、自国の金融ルールが国際経済・貿易ルールに適合し、現在の対外開放 ...

中国人民大学重陽金融研究院チーフエコノミストの廖群氏が円卓討論に出席し、参加した。 米国経済をどう見るかについては、米国経済の下振れは肯定的であり、悪化中で ...

香港の中信嘉華銀行の廖群・第1副総裁はこのほど、当面の中国経済にとって最大の問題は、通貨インフレではなく過剰投資であるとの見方を明らかにした。その上で、……

2009/10/8 -余永定(Yu Yongding)氏ご略歴 ... 中国の著名なエコノミストの1人。1969年中国科学院北京科学技術学院卒業後、1979年中国社会科学院入所。中国社会科学院 ...

| ||||||||||||||||||||||||

しかし、光大証券のチーフエコノミスト、Xu Gao氏のように、企業の高い借り入れコストを押し下げるために預金準備率を下げる可能性はかなり高い、との見方もでている。

2014/4/1 -光大証券(北京)のチーフエコノミスト、Xu Gao氏は「静かに(措置導入を)進めている。刺激策という言葉は後ろ向きな印象を与えるため、使えない」と ...

https://www.pekingnology.com/p/senior-chinese-finance-official-modern

2022

Senior Chinese finance official: Modern Monetary Theory exacerbates inequality

SAFE deputy head LU Lei on MMT

Reflecting the wide interest of your Pekingnologist and the dire need to bring more quality China content to the English-language part of the world, this is a newsletter that covers a lot of subjects. Today, it is a translation of an article about MMT, or Modern Monetary Theory.

It was published in the beginning of 2022 on 中国金融 China Finance, a bi-weekly magazine under the People’s Bank of China, China’s central bank. The author is 陆磊 LU Lei, Deputy Administrator of the State Administration of Foreign Exchange (SAFE) since June 2017. Prior to that, Lu served as the head of the Financial Stability Bureau (August 2016 to June 2017) and head of the Research Bureau (March 2014 to August 2016) of the central bank.

There have been numerous discussions on MMT in the English-language press in the recent several years, and it appears to your Pekingnologist that there haven’t been many Chinese voices, so the view from a current senior financial official in the second-largest economy should be a contribution.

What’s also interesting is that Lu apparently believes MMT - or at least the essence of it - has already been incorporated in the policies of the United States and Japan, despite MMT being more often described as “a niche theory endorsed by only a small but vocal group of far-left economists” and shunned by “mainstream but left-leaning economists” such as Lawrence Summers and Paul Krugman, who dismissed it as “just obviously indefensible”.

To help make Pekingnology sustainable, please consider buy me a coffee or pay me via Paypal.

The Practice and Effects on Distribution of Modern Monetary Theory in Developed Economies

Since the 18th National Congress of the Communist Party of China, the Central Committee of the CPC has given greater importance to gradually achieving common prosperity in view of the new changes in China’s development stage. Looking abroad, the world’s leading developed economies, represented by Japan and the United States, have adopted a “dual expansion” policy that combines loose monetary policy and expansionary fiscal policy in recent years. Indeed, the combination has restrained a rapid economic downturn but has also had a significant effect on distribution.

The widening gap between the rich and the poor has ignited extensive discussions. That Modern Monetary Theory (MMT) and Capital in the Twenty-First Century have attracted great attention shows that theories actually mirror the reality on the ground. The practice in major developed economies demonstrates that the redistributive effects of changes in the price structure should be considered.

The reintroduction of MMT is due to mainstream theory's failure to explain current economic and financial phenomenonSince the 1990s, post-Keynesian economists have developed the traditional state theory of money and put forward the concept of MMT. MMT has long been an obscure, niche theory, but after the 2008 global financial crisis, it became a hot topic discussed by people from many circles in developed economies, mainly attributable to the two following reasons.

First, the mainstream theory is incapable of explaining the current economic phenomenon of “easy money and low interest rate”. Reflections on the Great Depression fueled the rise of the Keynesian school in the 1930s, and government intervention in the economy through monetary and fiscal policy became the mainstream.

In the 1970s, the stagflation in major economies put the Keynesian policies in a dilemma over inflation and unemployment. The monetarist theory argued that the government should refrain from intervening, emphasizing that fluctuations in money supply were the fundamental cause of price changes. Since the global financial crisis in 2008, major developed economies have adopted ultra-loose monetary policies and expansionary fiscal policies, with rising government debts and persistently low interest rates. The stubborn phenomenon of “easy monetary policy, low interest rates, and low inflation” makes an explanation by the mainstream theory difficult.

Second, MMT to some extent explains the facts such as rising government debt and low inflation in developed economies. One of MMT’s pillars is functional finance, which attempts to achieve full employment without inflation. As an extension of Keynesian ideas in the monetary realm, MMT proposes that the central bank should support expansionary fiscal policy through monetary policy, allowing the government to have a more flexible fiscal policy without being constrained by institutional fiscal limitations.

[MMT argues that] To address economic woes and achieve full employment, central banks can inject liquidity into the market by purchasing government bonds and at the same time reduce the costs of government debt financing to increase the government’s solvency. [MMT argues that] At the level of fiscal spending that achieves full employment, rising government debt and liquidity expansion will not trigger hyperinflation. From a theoretical standpoint, a low-interest rate influences employment and factors of production, helps increasing the proportion of primary distribution in the distribution of national income, and expansionary fiscal policies obviously have effects on redistribution.

The world’s major central banks' practice of MMT enables a transfer of debts from the private sector to the government sector.The Bank of Japan implemented quantitative easing (QE) for the first time in the world, boosting the development of MMT by putting it into practice. Since the 1990s, the Japanese economy, from the burst of the asset bubble, began to descend into a long-term economic stagnation, and the Japanese policy rate approached the lower bound of zero from 1991 to 1999. Low-interest rates did not revitalize Japan’s economic growth. In March 2001, the Bank of Japan decided to implement QE when the interest rate approached zero. The Bank of Japan’s balance sheet expanded by 50 percent when it quited QE in the second quarter of 2006.

Japan further put MMT into practice after the 2008 international financial crisis. At the end of 2008, the Bank of Japan launched the second round of QE, expanding the yearly purchase of government bonds from 14.4 trillion yen to 16.8 trillion yen, and including a wider range of bonds such as 30-year bonds and floating-rate bonds into its purchases.

In the QE3 since 2013, there was an obvious trend of simultaneous growth in the Bank of Japan’s total assets and the purchase of government bonds. The central bank’s balance sheet soared from 157.9 trillion yen in early 2013 to 573.1 trillion yen by the end of 2019, an increase of 2.7 times. Since the outbreak of COVID-19, the size of government bonds held by the Bank of Japan further swelled. As of November 30, 2021, the Bank of Japan held 529.5 trillion yen in government bonds, accounting for 73 percent of its total assets and about half of the total outstanding government bonds.

Following the global financial crisis in 2008 which stimulated heated discussion on MMT, the Federal Reserve initiated putting the MMT into practice. Since the Federal Reserve launched its QE in 2008, it has not only supported the expansion of government debt financing demand but also kept inflation at a low level. The rising debts did not lead to the “economic collapse” that some economists were worried about. Some U.S. politicians became proponents of MMT, further promoting the practice of the MMT.

In response to the impact of the COVID-19 pandemic, the Federal Reserve increased its purchase of government bonds on a large scale, pushing its balance sheet expansion to an unprecedented level. As of December 1, 2021, the size of the Fed’s balance sheet hit an all-time high of 8.6 trillion U.S. dollars, which includes 5.6 trillion U.S. dollars in Treasuries, accounting for 65 percent of the total assets.

The European Central Bank also put into practice the MMT after the European debt crisis. The Eurozone began accelerated QE in 2014 across the board, and the balance sheet size of the European Central Bank rose from 2 trillion euros in September 2014 to 4.7 trillion euros in early 2019. Following the outbreak of COVID-19 in Europe in 2020, QE in the Eurozone picked up again. By November 2021, the balance sheet of the European Central Bank reached 8.4 trillion euros, up by 79 percent from the end of 2019.

Monetary policy in developed economies increases global inequality in distribution through the price structureGlobal wealth inequality hit new highs in recent years. According to the World Inequality Report 2022 released by the World Inequality Lab on December 7, 2021, about 2,750 billionaires control 3.5 percent of the world’s wealth, which is far higher than 1995 - just one percent in that year. The quickest growth rate happened after the outbreak of COVID-19. Inequality is caused by a host of reasons, and economic policies, including monetary policy, are important reasons.

Although the “dual expansion” of monetary and fiscal policies of developed economies have prevented economic collapse and worsening crises, they have brought in the rapid increase of financial asset prices and commodity prices. The difference between PPI and CPI has widened significantly. Changes in relative prices in the price structure have had significant effects on distribution for people at different stratas of society, exacerbating inequality. Specifically, there are three aspects:

First, rising financial asset prices brought more to the rich. Stimulated by unlimited QE, the three major indexes of the U.S. stock market have repeatedly hit record highs. After Federal Reserve Chairman Jerome Powell announced the plan to reduce the balance sheet in early November 2021, the U.S. stock market did not retract significantly but instead hit a new high for the year. Financial assets such as stocks account for a larger proportion of wealthy families’ assets, who are more dependent on income from capital. Rising financial asset price benefitted the rich more.

Second, the rapid rise of PPI is good news for upstream business oligarchs. In the meantime, a higher growth rate of PPI, compared to the CPI, further reduces the profitability of small and medium-sized enterprises (SMEs). Due to factors such as the pandemic and energy shortages, the prices of some commodities have been increasing.

According to the IMF Primary Commodity Prices, since May 2020, international commodity prices have risen by over 70 percent, with simultaneous increases for metals, food, and energy products. The U.S. Commodity Research Bureau Index grew by as high as 64.8 percent from the low point at the end of April 2020 to early November 2021, and it has remained high recently. Commodity prices pushed up the PPI as a whole. In October 2021, the PPI in the United States increased by 22.2 percent year-on-year, and the PPI in the Eurozone in October 2021 rose by 21.9 percent year-on-year. The profits generated by the rising prices of commodities such as raw materials are mostly reaped by the upstream oligarchs that control the resources. In comparison, SMEs have to bear the rising production costs. Moreover, the difference between PPI and CPI does not result in a simultaneous increase in the income of SMEs, so their profit was being eroded.

Third, the real income of residents decreases when the CPI continues to climb. Inflationary pressures were significant in major developed economies in 2021. The CPI in the United States increased by 6.2 percent year-on-year in October 2021, reaching a new high since November 1990. Germany’s CPI in November 2021 rose by 5.2 percent year-on-year, hitting a new high since 1992.

Inflation in the world’s major countries will peak at 5 percent, according to the OECD Economic Outlook released on December 1, 2021, before gradually falling to approximately 3 percent in 2023. High inflation raises the living cost of the general public and diminishes real purchasing power. Because nominal wage adjustment generally lags behind that of prices, high inflation has a greater impact on the lower-middle-income groups, who mainly rely on wages as income. According to the findings of a study released in late October 2021 by the Peterson Institute for International Economics, inflated-adjusted compensation - nominal compensation, wages and benefits - in the US was 0.6 percent lower than it was in December 2019.

Issac Newton wrote the Mathematical Principles of Natural Philosophy in 1687, in which the second, fifth, and seventh chapters of the second volume concern the law of viscosity of fluids, which was converted into differential equation by Daniel Bernoulli and Leonhard Euler in 1738. In 1822 and 1845, Claude-Louis Navier and George Gabriel Stokes put forward the nonlinear equations of “convective form” and “pressure gradient” at the molecular level. That could be an inspiration for us: the impact of monetary policy on various sectors is inconsistent, and there is a mutual viscous force between sectors.

This could help explain the relative movement of “monetary policy - reflection on asset prices - commodity market - PPI - CPI”. The monetary system on the gold standard can be understood as classical fluid mechanics. Contemporary monetary policy may need to be understood from the standpoint of turbulence theory.

The Sixth Plenary Session of the 19th CPC Central Committee emphasized deepening reform and opening up across the board and promoting common prosperity. Financial support for common prosperity is multi-dimensional, and inclusive finance, digitization, and differentiated reserve requirements are good practices. Essentially, the lessons from various countries indicate that the impact on income and wealth effect by monetary policy via “asset prices - commodity prices - consumer prices” must not be overlooked. Given the combined impacts of the changes unseen in a century and the pandemic, how to optimize distribution is a major theoretical and practical issue the world has to face. There is also room for further optimizing economic policies such as monetary and fiscal policies.

(This article is based on the keynote speech delivered by the author Lu Lei at the 2021中国金融学会学术年会 “2021 Annual Conference of China Society for Finance & Banking” held on December 11, 2021)

To help make Pekingnology sustainable, please consider buy me a coffee or pay me via Paypal.

《《発行达经济体现代货币処理论实慣及分配效应发达经济体现代货币理论实践及分配效应》》

先進国における現代貨幣理論の実践と分配への影響The Practice and Effects on Distribution of Modern Monetary Theory in Developed Economies

中国共産党第18回党大会以来、中国共産党中央委員会は、中国の発展段階の新たな変化を踏まえ、共同繁栄を徐々に達成することをより重視してきている。海外に目を向けると、日本や米国に代表される世界の先進国は近年、緩和的な金融政策と拡張的な財政政策を組み合わせた「二元的拡大」政策を採用しています。実際、この組み合わせは急速な経済低迷を抑制したが、流通にも重大な影響を与えた。Since the 18th National Congress of the Communist Party of China, the Central Committee of the CPC has given greater importance to gradually achieving common prosperity in view of the new changes in China’s development stage. Looking abroad, the world’s leading developed economies, represented by Japan and the United States, have adopted a “dual expansion” policy that combines loose monetary policy and expansionary fiscal policy in recent years. Indeed, the combination has restrained a rapid economic downturn but has also had a significant effect on distribution.

富裕層と貧困層の間の格差の拡大は広範な議論を引き起こしている。現代貨幣理論 (MMT) とThe widening gap between the rich and the poor has ignited extensive discussions. That Modern Monetary Theory (MMT) and 21 世紀の資本がCapital in the Twenty-First Century大きな注目を集めていることは、理論が実際に現場の現実を反映していることを示しています。主要先進国における慣行は、価格構造の変化による再分配効果を考慮すべきであることを示しています。 have attracted great attention shows that theories actually mirror the reality on the ground. The practice in major developed economies demonstrates that the redistributive effects of changes in the price structure should be considered.

The reintroduction of MMT is due to mainstream theory's failure to explain current economic and financial phenomenon1990 年代以降、ポストケインズ経済学者は伝統的なSince the 1990s, post-Keynesian economists have developed the traditional 貨幣国家理論を発展させstate theory of money、MMT の概念を提唱しました。 MMT は長らく曖昧でニッチな理論でしたが、2008 年の世界金融危機後、主に次の 2 つの理由により、先進国の多方面で議論されるホットなテーマとなりました。 and put forward the concept of MMT. MMT has long been an obscure, niche theory, but after the 2008 global financial crisis, it became a hot topic discussed by people from many circles in developed economies, mainly attributable to the two following reasons.

まず、主流の理論は「お金が楽で低金利」という現在の経済現象を説明することができません。大恐慌への反省から 1930 年代にケインズ学派の台頭が促進され、金融政策と財政政策を通じた政府の経済介入が主流になりました。First, the mainstream theory is incapable of explaining the current economic phenomenon of “easy money and low interest rate”. Reflections on the Great Depression fueled the rise of the Keynesian school in the 1930s, and government intervention in the economy through monetary and fiscal policy became the mainstream.

1970年代、主要国のスタグフレーションにより、ケインズ政策はインフレと失業をめぐるジレンマに陥った。マネタリストIn the 1970s, the stagflation in major economies put the Keynesian policies in a dilemma over inflation and unemployment. The 理論は、monetarist theory貨幣供給量の変動が価格変動の根本的な原因であることを強調し、政府は介入を控えるべきだと主張した。 2008年の世界金融危機以来、主要先進国は超緩和的な金融政策と拡張的な財政政策を採用しており、政府債務が増加し、低金利が続いている。 「金融緩和政策、低金利、低インフレ」という頑固な現象は、主流理論による説明を困難にしています。 argued that the government should refrain from intervening, emphasizing that fluctuations in money supply were the fundamental cause of price changes. Since the global financial crisis in 2008, major developed economies have adopted ultra-loose monetary policies and expansionary fiscal policies, with rising government debts and persistently low interest rates. The stubborn phenomenon of “easy monetary policy, low interest rates, and low inflation” makes an explanation by the mainstream theory difficult.

第二に、MMTは先進国における政府債務の増加や低インフレなどの事実をある程度説明している。 MMT の柱の 1 つはSecond, MMT to some extent explains the facts such as rising government debt and low inflation in developed economies. One of MMT’s pillars is 、インフレなしで完全雇用を達成しようとする機能的金融です。functional finance金融分野におけるケインズ主義の考え方の延長として、MMTは、中央銀行が金融政策を通じて拡張的な財政政策を支援し、政府が制度的な財政制限に制約されることなくより柔軟な財政政策を行えるようにすべきであると提案しています。, which attempts to achieve full employment without inflation. As an extension of Keynesian ideas in the monetary realm, MMT proposes that the central bank should support expansionary fiscal policy through monetary policy, allowing the government to have a more flexible fiscal policy without being constrained by institutional fiscal limitations.

[MMTはこう主張する] 経済危機に対処し、完全雇用を達成するために、中央銀行は国債を購入することで市場に流動性を注入し、同時に政府の債務調達コストを削減して政府の支払い能力を高めることができる。 [MMTはこう主張する] 完全雇用を達成する財政支出のレベルでは、政府債務の増加と流動性の拡大はハイパーインフレを引き起こすことはない。理論的観点から見ると、低金利は雇用と生産要素に影響を与え、国民所得の分配における一次分配の割合の増加に役立ち、拡張的な財政政策は明らかに再分配に影響を及ぼします。[MMT argues that] To address economic woes and achieve full employment, central banks can inject liquidity into the market by purchasing government bonds and at the same time reduce the costs of government debt financing to increase the government’s solvency. [MMT argues that] At the level of fiscal spending that achieves full employment, rising government debt and liquidity expansion will not trigger hyperinflation. From a theoretical standpoint, a low-interest rate influences employment and factors of production, helps increasing the proportion of primary distribution in the distribution of national income, and expansionary fiscal policies obviously have effects on redistribution.

The world’s major central banks' practice of MMT enables a transfer of debts from the private sector to the government sector.日本銀行は世界で初めて量的緩和(QE)を実施し、MMTの実践を通じてMMTの発展を促進した。 1990年代以降、日本経済は資産バブルの崩壊から長期経済停滞に陥り始め、1991年から1999年にかけて日本の政策金利はゼロの下限に近づきました。低金利は活性化しませんでした。日本の経済成長。 2001年3月、日本銀行は金利がゼロに近づいた際に量的緩和の実施を決定した。 2006 年第 2 四半期に量的金融緩和を解除したとき、日銀のバランスシートは 50% 拡大しました。 The Bank of Japan implemented quantitative easing (QE) for the first time in the world, boosting the development of MMT by putting it into practice. Since the 1990s, the Japanese economy, from the burst of the asset bubble, began to descend into a long-term economic stagnation, and the Japanese policy rate approached the lower bound of zero from 1991 to 1999. Low-interest rates did not revitalize Japan’s economic growth. In March 2001, the Bank of Japan decided to implement QE when the interest rate approached zero. The Bank of Japan’s balance sheet expanded by 50 percent when it quited QE in the second quarter of 2006.

日本は2008年の国際金融危機後、MMTをさらに実践した。 2008年末、日本銀行は量的緩和第2弾を開始し、年間国債購入額を14.4兆円から16.8兆円に拡大し、30年債や変動利付債などより幅広い国債を対象とした。債券を購入に組み込む。Japan further put MMT into practice after the 2008 international financial crisis. At the end of 2008, the Bank of Japan launched the second round of QE, expanding the yearly purchase of government bonds from 14.4 trillion yen to 16.8 trillion yen, and including a wider range of bonds such as 30-year bonds and floating-rate bonds into its purchases.

2013年以降のQE3では、日銀の総資産の増加と国債の購入が同時に進むという明らかな傾向が見られた。中銀のバランスシートは2013年初めの157.9兆円から2019年末には573.1兆円と2.7倍に急増した。新型コロナウイルス感染症の発生以降、日銀が保有する国債の規模はさらに膨らんだ。 2021年11月30日時点で日銀が保有する国債は529.5兆円で、総資産の73%、国債発行残高の約半分を占める。In the QE3 since 2013, there was an obvious trend of simultaneous growth in the Bank of Japan’s total assets and the purchase of government bonds. The central bank’s balance sheet soared from 157.9 trillion yen in early 2013 to 573.1 trillion yen by the end of 2019, an increase of 2.7 times. Since the outbreak of COVID-19, the size of government bonds held by the Bank of Japan further swelled. As of November 30, 2021, the Bank of Japan held 529.5 trillion yen in government bonds, accounting for 73 percent of its total assets and about half of the total outstanding government bonds.

2008 年の世界金融危機により MMT に関する激しい議論が巻き起こった後、連邦準備制度は MMT の実践を開始しました。 FRBは2008年に量的緩和を開始して以来、政府債務による資金調達需要の拡大を支援しただけでなく、インフレを低水準に維持してきました。債務の増加は一部のエコノミストが懸念していた「経済崩壊」には至らなかった。米国の一部の政治家はMMTの支持者となり、MMTの実践をさらに推進した。Following the global financial crisis in 2008 which stimulated heated discussion on MMT, the Federal Reserve initiated putting the MMT into practice. Since the Federal Reserve launched its QE in 2008, it has not only supported the expansion of government debt financing demand but also kept inflation at a low level. The rising debts did not lead to the “economic collapse” that some economists were worried about. Some U.S. politicians became proponents of MMT, further promoting the practice of the MMT.

新型コロナウイルス感染症のパンデミックの影響に対応して、連邦準備理事会は大規模な国債買い入れを拡大し、バランスシートの拡大を前例のない水準に押し上げた。 2021年12月1日時点で、FRBのバランスシートの規模は過去最高の8.6兆ドルに達し、このうち5.6兆ドルの国債が総資産の65%を占めている。In response to the impact of the COVID-19 pandemic, the Federal Reserve increased its purchase of government bonds on a large scale, pushing its balance sheet expansion to an unprecedented level. As of December 1, 2021, the size of the Fed’s balance sheet hit an all-time high of 8.6 trillion U.S. dollars, which includes 5.6 trillion U.S. dollars in Treasuries, accounting for 65 percent of the total assets.

欧州中央銀行も欧州債務危機後にMMTを実践した。ユーロ圏は2014年に全面的に量的金融緩和の加速を開始し、欧州中央銀行のバランスシート規模は2014年9月の2兆ユーロから2019年初めには4兆7,000億ユーロに増加した。2020年に欧州で新型コロナウイルス感染症が発生したことを受けて、量的金融緩和は2014年に欧州で発生した。ユーロ圏では再び持ち直した。欧州中央銀行のバランスシートは2021年11月までに8兆4000億ユーロに達し、2019年末から79%増加した。The European Central Bank also put into practice the MMT after the European debt crisis. The Eurozone began accelerated QE in 2014 across the board, and the balance sheet size of the European Central Bank rose from 2 trillion euros in September 2014 to 4.7 trillion euros in early 2019. Following the outbreak of COVID-19 in Europe in 2020, QE in the Eurozone picked up again. By November 2021, the balance sheet of the European Central Bank reached 8.4 trillion euros, up by 79 percent from the end of 2019.

Monetary policy in developed economies increases global inequality in distribution through the price structure世界の富の不平等は近年、新たな最高値を記録した。世界不平等Global wealth inequality hit new highs in recent years. According to the 研究所が2021年12月7日に発表した「世界不平等報告書2022年版」World Inequality Report 2022によると、約2750人の億万長者が世界の富の3.5%を支配しているが、これは1995年よりもはるかに高く、同年はわずか1%だった。最も急速な成長率は、新型コロナウイルス感染症の発生後に発生した。不平等はさまざまな理由によって引き起こされますが、金融政策を含む経済政策が重要な理由です。 released by the World Inequality Lab on December 7, 2021, about 2,750 billionaires control 3.5 percent of the world’s wealth, which is far higher than 1995 - just one percent in that year. The quickest growth rate happened after the outbreak of COVID-19. Inequality is caused by a host of reasons, and economic policies, including monetary policy, are important reasons.

先進国の金融政策と財政政策の「二重の拡大」は経済崩壊と危機の深刻化を防いだものの、金融資産価格と商品価格の急速な上昇をもたらした。 PPIとCPIの差は大幅に拡大した。価格構造における相対価格の変化は、社会のさまざまな階層の人々の分配に重大な影響を及ぼし、不平等を悪化させています。具体的には、次の 3 つの側面があります。Although the “dual expansion” of monetary and fiscal policies of developed economies have prevented economic collapse and worsening crises, they have brought in the rapid increase of financial asset prices and commodity prices. The difference between PPI and CPI has widened significantly. Changes in relative prices in the price structure have had significant effects on distribution for people at different stratas of society, exacerbating inequality. Specifically, there are three aspects:

まず、金融資産価格の上昇は富裕層にさらなる恩恵をもたらした。無制限の量的緩和に刺激され、米国株式市場の主要3指数は過去最高値を繰り返し更新している。ジェローム・パウエル連邦準備制度理事会議長が2021年11月First, rising financial asset prices brought more to the rich. Stimulated by unlimited QE, the three major indexes of the U.S. stock market have repeatedly hit record highs. After Federal Reserve Chairman Jerome Powell announced the plan to reduce the balance sheet in 初旬earlyにバランスシート削減計画を発表した後、米国株式市場は大きく後退せず、むしろ年初高値を更新した。資本収入への依存度が高い裕福な家庭では、株式などの金融資産が資産の大きな割合を占めている。金融資産価格の上昇は富裕層にさらに恩恵をもたらしました。 November 2021, the U.S. stock market did not retract significantly but instead hit a new high for the year. Financial assets such as stocks account for a larger proportion of wealthy families’ assets, who are more dependent on income from capital. Rising financial asset price benefitted the rich more.

第二に、PPI の急速な上昇は、上流のビジネス寡頭企業にとって朗報です。一方、CPI と比較して PPI の高い成長率は、中小企業 (SME) の収益性をさらに低下させます。パンデミックやエネルギー不足などの要因により、一部の商品の価格が上昇しています。Second, the rapid rise of PPI is good news for upstream business oligarchs. In the meantime, a higher growth rate of PPI, compared to the CPI, further reduces the profitability of small and medium-sized enterprises (SMEs). Due to factors such as the pandemic and energy shortages, the prices of some commodities have been increasing.

According to the IMF 一次産品価格IMF Primary Commodity Pricesによると、2020 年 5 月以降、国際商品価格は 70% 以上上昇し、同時に金属、食品、エネルギー製品も上昇しました。米国, since May 2020, international commodity prices have risen by over 70 percent, with simultaneous increases for metals, food, and energy products. The U.S. 商品調査局指数はCommodity Research Bureau Index2020年4月末の安値から2021年11月初旬までに64.8%もの上昇率を示し、最近も高水準が続いている。コモディティ価格がPPI全体を押し上げた。 2021年10月の米国のPPIは grew by as high as 64.8 percent from the low point at the end of April 2020 to early November 2021, and it has remained high recently. Commodity prices pushed up the PPI as a whole. In October 2021, the PPI in the United States increased by 前年比22.2%上昇し、2021年10月のユーロ圏のPPIは22.2 percent前年比21.9%上昇した。原材料など商品価格の上昇によって生み出される利益のほとんどは、資源を支配する上流の寡頭政治家によってもたらされる。それに比べて、中小企業は生産コストの上昇を負担しなければなりません。さらに、PPI と CPI の差は中小企業の収入の増加を同時にもたらさないため、中小企業の利益が侵食されていました。 year-on-year, and the PPI in the Eurozone in October 2021 rose by 21.9 percentyear-on-year. The profits generated by the rising prices of commodities such as raw materials are mostly reaped by the upstream oligarchs that control the resources. In comparison, SMEs have to bear the rising production costs. Moreover, the difference between PPI and CPI does not result in a simultaneous increase in the income of SMEs, so their profit was being eroded.

第三に、CPIが上昇し続けると住民の実質所得が減少する。 2021 年の主要先進国ではインフレ圧力が顕著でした。2021 年 10 月の米国の CPI は前年比 6.2% 上昇し、Third, the real income of residents decreases when the CPI continues to climb. Inflationary pressures were significant in major developed economies in 2021. The CPI in the United States increased by 19906.2年 11 月以来の最高値に達しました。2021 年 11 月のドイツの CPI は percent year-on-year in October 2021, reaching a new high since November 1990. Germany’s CPI in November 2021 rose by 前年比5.2%上昇しました。5.2 percent年、1992年以来の新高値を記録した。 year-on-year, hitting a new high since 1992.

Inflation in the world’s major countries will peak at 5 percent, according to the 2021年12月1日に発表されたOECD経済見通しOECD Economic Outlookによると、世界の主要国のインフレ率は5%でピークに達し、2023年には約3%まで徐々に低下すると予想されています。高インフレは一般大衆の生活費を上昇させ、実質購買力を減少させます。 。名目賃金の調整は一般に物価の調整よりも遅れているため、インフレ率の上昇は、主に収入として賃金に依存している下位中所得層に大きな影響を与えます。ピーターソン国際経済研究所が2021年10月下旬に発表した released on December 1, 2021, before gradually falling to approximately 3 percent in 2023. High inflation raises the living cost of the general public and diminishes real purchasing power. Because nominal wage adjustment generally lags behind that of prices, high inflation has a greater impact on the lower-middle-income groups, who mainly rely on wages as income. According to the findings of a 調査study結果によると、米国における水増し調整後の報酬(名目報酬、賃金、福利厚生)は、2019年12月と比べて0.6%減少した。 released in late October 2021 by the Peterson Institute for International Economics, inflated-adjusted compensation - nominal compensation, wages and benefits - in the US was 0.6 percent lower than it was in December 2019.

アイザック・ニュートンは1687 年にIssac Newton wrote the 『自然哲学の数学的原理』Mathematical Principles of Natural Philosophyを書きました。その第 2 巻の第 2 章、第 5 章、および第 7 章は流体の粘性の法則に関係しており、この法則は 1738 年にダニエル・ベルヌーイとレオンハルト・オイラーによって微分方程式に変換されました。 1822 年と 1845 年に、クロード・ルイ・ナビエとジョージ・ガブリエル・ストークス in 1687, in which the second, fifth, and seventh chapters of the second volume concern the law of viscosity of fluids, which was converted into differential equation by Daniel Bernoulli and Leonhard Euler in 1738. In 1822 and 1845, Claude-Louis Navier and George Gabriel Stokes put forward the は、分子レベルでの「対流形式」と「圧力勾配」の非線形方程式nonlinear equationsを提唱しました。それは私たちにとってインスピレーションとなるかもしれません。さまざまなセクターに対する金融政策の影響には一貫性がなく、セクター間には相互に粘性のある力が存在します。 of “convective form” and “pressure gradient” at the molecular level. That could be an inspiration for us: the impact of monetary policy on various sectors is inconsistent, and there is a mutual viscous force between sectors.

これは、「金融政策 - 資産価格への反映 - 商品市場 - PPI - CPI」の相対的な動きを説明するのに役立つ可能性があります。金本位制の通貨制度は古典的な流体力学として理解できます。現代の金融政策はThis could help explain the relative movement of “monetary policy - reflection on asset prices - commodity market - PPI - CPI”. The monetary system on the gold standard can be understood as classical fluid mechanics. Contemporary monetary policy may need to be understood from the standpoint of 乱流理論turbulenceの観点から理解する必要があるかもしれません。 theory.

第19期中国共産党中央委員会第6回総会は、全面的な改革開放の深化と共同繁栄の促進を強調した。共通の繁栄のための財政的支援は多面的であり、包括的な財政、デジタル化、およびThe Sixth Plenary Session of the 19th CPC Central Committee emphasized deepening reform and opening up across the board and promoting common prosperity. Financial support for common prosperity is multi-dimensional, and inclusive finance, digitization, and 差別化された準備金要件がdifferentiated reserve requirements良い実践です。基本的に、各国の教訓は、金融政策による「資産価格-商品価格-消費者物価」を通じた所得と are good practices. Essentially, the lessons from various countries indicate that the impact on income and 資産効果への影響wealth effectを看過してはならないことを示している。過去 1 世紀に見られなかった変化とパンデミックの複合的な影響を考慮すると、流通をどのように最適化するかは、世界が直面しなければならない大きな理論的かつ実践的な問題です。金融政策や財政政策などの経済政策をさらに最適化する余地もある。 by monetary policy via “asset prices - commodity prices - consumer prices” must not be overlooked. Given the combined impacts of the changes unseen in a century and the pandemic, how to optimize distribution is a major theoretical and practical issue the world has to face. There is also room for further optimizing economic policies such as monetary and fiscal policies.

(This article is based on the keynote (この記事は、2021年12月11日に開催された2021年中国金融学会学术年会「2021 Annual Conference of China Society for Finance & Banking」における著者の陸磊氏の基調講演speechを基にしています) delivered by the author Lu Lei at the 2021中国金融学会学术年会 “2021 Annual Conference of China Society for Finance & Banking” held on December 11, 2021)

https://www.tandfonline.com/doi/full/10.1080/10971475.2024.2319408?src=exp-la

An MMT Informed Fiscal Reform for China

Employing the Modern Monetary Theory (MMT), this paper examines the current Chinese fiscal system and highlights its three characteristics. First, fiscal revenues are centralized at the central government while expenditures are decentralized at the local governments; second, fiscal spending focuses on public investment but is insufficient in providing social safety net and public services; and third, indirect tax accounts for a great majority of tax revenues, leading to limited progressivity of the tax system. These limitations have constrained the effectiveness of China’s fiscal policies and generated many perverse impacts. With the understanding that the central government has the monetary sovereignty and does not face financing constrained and that taxes are not to raise revenues for fiscal spending but to serve other purposes, the paper calls for fiscal reforms that realign fiscal resources and spending responsibilities between the central and local governments, increase fiscal spending on social security and public services, as well as broaden personal income tax to improve the distributive effect of taxation.

1 China is a unitary state with a multi-tiered government structure. Subnational governments are in principle agents of the central government, tasked with carrying out national policy objectives within their own jurisdictions.

2 Local governments can be further divided into provinces, prefectures, counties, and townships. County governments are responsible for the largest expenditure responsibility. Their revenues account for less than 5% of GDP but expenditure takes up 9% of GDP in 2014 (Wingender, 2018).

3 There are four budgets for the governments, including the general public budget (GPB), the social security fund, the government fund budget (with 24 government funds, the largest of which is the land lease fund), and the state own enterprise operation fund budget. The four budgets account for 52.6%, 23%, 23.3% and 1.1% of the total government budgets, respectively. Surplus from the government fund budget and the state owned enterprise operation fund budget can be transferred to the general public budget to finance public services, while the financing gap of the social security fund budge can be filled by transfers from the general public budget (See Qiao et al., 2022).

4 The majority of the Social Security spending is not part of the general public budget but included in the social security fund budget. What is included in the general public budget are mostly administrative costs of social insurance, employment and labor relations managements, and others.

5 Local governments transfer public assets such as land or shares of public facilities as capital, and use LGFVs to issue bonds or borrow loans from banks or other financial institutions. The funds raised through LGFVs are typically used for infrastructure investments and other fiscal expenditures.

6 One major cause for the rapid expansion of LGFVs borrowing was due to the 4 trillion yuan stimulus package the central government launched in 2008 in response to the Global Financial Crisis. Local governments were responsible for 70% of the spending but without the adequate fiscal resources, they resorted to LGFVs to raise funds for infrastructure spending (see Liang, 2016a, 2016b).

7 Using US$1 = 7 yuan throughout the paper.

8 Local governments were prohibited from issuing bonds on their own before 2014, except for a five-year pilot program that started in 2009, where the Ministry of Finance issued RMB 200 billion in local government bonds on behalf of local governments. The central government later allowed a small number of provincial governments to issue bonds directly (about 3 billion yuan to 4 billion yuan as of the end of 2014) (Lam, 2019).

9 Based on the IMF’s measure of “augmented deficit and debt”, local government debt in China reached 66 trillion yuan ($9.4 trillion) as of 2022. IMF’s estimates include the land sales proceeds as part of the local government debt because it conceives of the reduction in assets as equivalent as an increase in debt. Yu (2023) discredits this computation.

10 Local governments focus on promoting economic growth because their political careers are tied to the economic performance of their jurisdictions. This kind of local government competition tournament on the one hand promotes economic growth but on the other hand, lead to over and repetitive investments in some areas and heighten the local government debt problem, as well as the lack of spending on social programs and public services (see, e.g. Fu & Zhang, 2007; Liang & Li, 2016).

11 As mentioned above, pension is included in the social security fund budget. In 2020, the central social security fund revenue and expenditure were 858.4 billion yuan ($122.6 billion) and 857.8 billion yuan ($122.5 billion), respectively; the local government social security fund revenue and expenditure were 7928 billion yuan ($1132.6billion) and 8550.5 billion yuan ($1221.5 billion), respectively (Ministry of Finance, 2021).

12 For instance, Foxconn facilities in Zhengzhou fill 50% of its workforce with temporary workers in August 2019, violation of the 10% upper limit imposed by the Chinese Labor Law. Many of these temporary workers are not covered by social insurance, including pension. Zhengzhou government has the incentive to look away as Foxconn is a major employer and tax payer for the local economy. Many employers also under report wage levels to reduce pension contributions (OECD 2020).

13 Under China’s hukou (residential registration) system, rural workers can migrate to urban cities for jobs but they are still considered as rural residents and do not enjoy the same social services and benefits (e.g. public education and health care) as their rural counterparts. Migrant workers typically return to their rural residences if they can’t find jobs in the urban cities.

14 Similar to the pension scheme, for medical insurance, a contributory plan is set up for urban employees and the plan consists of social medial insurance and a mandatory individual account. Self-employed individuals could also purchase medical insurance plan. A separate plan would provide basic medical insurance for rural and non-salaried urban residents.

15 Including implicit debt services through the LGFVs, the interest payment could multiply to 20% of the total local government revenues.

16 There are mainly two main counterarguments against the central government involvement. One view holds that central government does not have sufficient fiscal resources to “bail out” local governments. It is clear, from the analysis here, that central government does not have a fiscal/financing constraint. Another view maintains that central government bailout could worsen local governments’ moral hazard. Be that as it may, there are dire consequences if local government debt overhang materializes. To improve local government’s fiscal responsibilities, it is more effective to work on local government officials’ incentives by including debt sustainability as one of the performance evaluation criterions (Zhang, 2023).

★★

https://spc.jst.go.jp/experiences/economy/economy_2360.html

【23-60】経済復興のカギはマクロコントロールモデルのイノベーション/劉尚希氏

閔 傑/『中国新聞週刊』記者 江 瑞/翻訳 2023年09月13日

中国財政科学研究院院長・劉尚希氏インタビュー

中国経済が全体として上向きに転じようとしている昨今だが、「外部環境が複雑さと厳しさを増し、世界の貿易投資が鈍化するなど、中国経済の回復に直接的影響を及ぼす要因が存在する」。

2023年6月16日に開かれた国務院常務会議では、経済の持続的好転を実現させるための一連の政策措置の検討・推進を進めていることが明らかにされた。

2023年の第2四半期以降、経済復興の勢いは当初の期待には及んでいない。中国財政科学研究院院長の劉尚希氏は、国民および企業の自信は最近になってやや上向いてきたものの、まだ不安定だと分析し、特に警戒しなければならないのは、「国民に根強く残る財布の紐を締める傾向が、再度の経済収縮を引き起こすリスクをはらんでいること」だと指摘する。

「目下、財政・通貨政策の信号は非常に明確ですが、その伝達がうまくいっていないため、体制や政策の刷新が必要です」。なかでもカギとなるのがマクロコントロールモデルの刷新であり、経済の下振れリスクに直面するなか、政府はマクロ政策や改革措置などの面で早急に新たな一手を打ち出すことが強く望まれる、と劉尚希氏は訴えた。

中国財政科学研究院院長・劉尚希氏。

「いくつもの要因が重なり、経済復興が困難さを増している」

記者:上半期の経済を振り返ると、復興は期待したほど進んでいないというのが一般的な認識かと思いますが、先生は上半期の経済情勢をどうご覧になりましたか。

劉尚希:復興は期待したほど進んでいない、これが皆さんの共通認識かと思います。元々、コロナ禍が終われば経済はすぐに盛り返すだろうという希望的観測が世間にありましたが、現実はそうはなっていません。一部の経済指標では、今年の第2四半期、つまり4月以降、経済の下振れ兆候が現れていました。それは即ち、リスクが拡散、拡大傾向にあるということを意味していると考えられ、それに反論する人はあまりいないと思われます。

経済下振れの原因は、いくつもの要因が重なっています。まず1つ目は、コロナ禍の「傷跡」です。長く続いたコロナ禍は、企業のバランスシートを大きく損ない、個人事業主や零細企業の経営にもダメージが及び、実質的に国民全体のバランスシートを崩す事態へと発展しました。これはコロナ禍が経済面に残した「爪痕」で、無視できない要因です。

2つ目は、不動産市場の下落による打撃です。不動産業は他産業との連関性が高く、「房住不炒」〔住宅は住むためのものであって、投機売買するためのものではない〕はまったくもって正しいことなのですが、それゆえ不動産業は、どうモデルチェンジしていくかということを模索している途中で、業界全体が調整中という状態です。その連関性の高さゆえ、不動産業自体はもちろんのこと、川上・川下の全ての産業、さらには金融や国民生活にも連鎖反応が及んでいます。例えば、不動産価格が下落し、不動産の資産価値が落ちていると感じた消費者が、地域によっては現在の資産価値を借入額が上回る状態になると、「ローン滞納」を選ぶ人々が出てきて、バランスシートが収縮する結果になっています。また、「3つのレッドライン」〔2020年8月に中国政府が打ち出した財務改善要求。①負債比率(Liability to Asset)を70%以下とする、②純負債資本倍率(Net DER)は1倍以下とする、③現預金短期有利子負債比率(Cash Coverage of ST Debt)を1倍以上とする、という3つの指標をクリアすることが求められた〕政策が打ち出されると、不動産業向けの金融政策に調整が入り、「住宅引渡し保証」が奨励されるようになりましたが、不動産デベロッパー自体ジリ貧のところが多く、バランスシートは大打撃を受けています。

3つ目は外部環境です。いまは世界的に需要不足で、グローバル経済は下振れ、衰退に向かっています。このことが、輸出への打撃や受注の減少といった形で表出し、中国経済の足を引っ張っていることは間違いありません。こうした外部要因が重なり中国経済の復興を妨げ、さらに経済の下振れを招いているのです。

4つ目は、監督管理の一貫性のなさを生む、政府と市場との関係です。これは大手デジタルプラットフォームだけでなく、各方面にも関係する問題です。数年前までの監督管理のやり方は、出し抜けに関連法が制定されるというもので、市場との意思疎通はまったく不十分でした。突然法令が制定されたことで生じた混乱の影響は、現在でもなお残っています。監督管理の強化は必要ですが、法治という軌道に沿って監督管理政策の一貫性を高めることが課題だと言えるでしょう。これは、市場の期待感を改善し安定させるために、非常に重要なことです。

さらにもう1つ、国営企業と民間企業との関係もあります。例えば不動産業を見てみると、両者ともに打撃を受けているとはいえ、民間不動産企業のダメージは非常に大きく、国営企業のダメージは相対的に小さいものとなっていますが、この差こそ、民間企業の自信のなさを表していると言えます。デジタル経済においては、民間企業がトップランナーでしたが、いまは息切れしている状態です。中央政府は繰り返し「2つの揺るがず」を強調し、民間経済の発展を支援してきましたが、実際のところ、公平な競争原則は、国営企業と民間企業との間で真に実現されていたとは言い難いものでした。何と言っても民間企業のほうが市場が大きいため、民間投資がマイナス成長に転じた場合、政府や国営企業による投資では支えきれません。現在の趨勢から見れば、もし民間経済がさらに収縮した場合、国民経済の下振れは加速するでしょう。

以上に挙げた要因は、単独で生じた場合、それほどの打撃にはなりませんが、同時かつ重なって生じた場合は、悪い相乗効果が発揮され、期待感の改善は難しくなります。中央経済工作会議は2年前の時点で中国経済が直面する「三重苦」を訴えていますが、現在に至ってもそれらは解決されていません。それゆえ、経済復興は、あたかも車輪がぬかるみにはまってなかなか抜け出せずにいるように、前途多難だと言えます。

記者:先生は以前、「国民に根強く残る財布の紐を締める傾向が、再度の経済収縮を引き起こすリスクをはらんでいる」と仰っていましたが、そのリスクはどの程度あるとお考えですか。

劉尚希:現在の中国経済は、岐路に立っている状態だと考えます。岐路と言ったのは、先ほど挙げたいくつかの要因は周期的なものではないからです。もし周期的な要因であれば、耐え忍んでいれば、経済は自ずと好転します。いま必要なのはリスク意識の強化。それから政府がマクロ政策や改革措置などの面で新たな一手を打ち出すことが強く望まれます。

現在は、復興の遅れではなく、より深部に問題が存在している状態です。また、メカニズムや構造的な問題が以前からあり、コロナ禍の3年間はその対応どころではなかったため、問題がさらに積み上がった感があり、その負の影響が経済情勢にも出てきています。いま早急に必要なのは、構造的な問題やメカニズムの問題に改革を断行することです。そうすれば中国経済はぬかるみから抜け出すことができるでしょう。

目下の経済状況に対し、政府がマクロ政策や改革措置などの面で新たな一手を打ち出し、経済の持続的好転を推し進めることが求められる。写真/視覚中国

「地方の緊縮的な財政運営は、中央の積極的な財政政策の効率向上要求と相容れない」

記者:先生は最近、「目下、財政・通貨政策のシグナルは非常に明確だが、その伝達がうまくいっていないため、体制や政策の刷新が必要」と仰っていましたが、これはどういう意味でしょうか。

劉尚希:主に政策上の話ですが、シグナルは非常に明確です。例えば、積極的な財政政策と穏健な通貨政策の実施というのははっきりしています。程度や効果についてはまた別の問題です。

程度が十分かどうかというのは、まず効果で判断しなければなりません。効果を見ずに程度だけを見ていては、逆の結果になってしまう恐れがあります。まず評価すべきは、財政および通貨政策の効果です。近年の様子を見ていると、財政・通貨政策の効果は、限界効用逓減の法則で、どんどん薄れてきています。その根本的原因は、財政・通貨政策の伝達は良好な体制基盤があってこそだからです。体制基盤に欠陥があればうまく伝達されませんし、体制が不健全であれば、伝達効果は大幅に削られてしまうのです。

現在の体制基盤は十分に健全だとは言えません。例えば金融分野では、通貨政策の体制基盤は金融体制によって決まるため、現代的な銀行制度を確立する必要があります。これが完全に確立されていないと、市場化を目標とする金融構造改革で成果を挙げたとしても、その中身が不明瞭になってしまいます。財政体制改革で進展があっても、中央と地方の財政関係改革は期待ほどは進みません。したがって、目下の地方の財政難は、中央と地方の財政関係の調整と切っても切れない関係にあるのです。

現行体制の下で、地方の緊縮的な財政運営は、中央の積極的な財政政策の効率向上要求と相容れないところがあるのかもしれません。たとえ全国の財政赤字を拡大しても、地方の債券規模を拡大しても、政策シグナルの伝達は阻害されてしまうでしょう。この他、通貨の伝達でも同様の問題が存在します。マネーサプライを大幅に増やし、マネーストックが経済成長速度をはるかに上回る二桁の伸びを記録している一方、預金がローンを上回る速度で増加し、マクロ上ではローンの「空回り」現象が生じているように見えます。

記者:通貨の伝達不足を解決するため、人民銀行は資金直達メカニズム、即ち構造性通貨政策を制定しました。現在のところ、その効果はいかほどなのでしょう。

劉尚希:構造性通貨政策は、一定方向の流動性の開放に依拠して実施されるもので、本質的には財政部門の仕事となり、財政政策の支援があってこそ効果を発揮するものです。目下のマネーサプライ政策は、効果がどんどん薄れ、企業および国民に対し「放水しようにも水が流れ出ていかない」状態になっています。企業の赤字は膨らみ、借り入れを望まない企業が増えています。これは国民も同じです。利下げは一定の効果を発揮しましたが、民間企業にとって、資本コストは依然高いと感じられるようです。

利下げのみに頼っていては根本的な問題を解決できません。カギとなるのは、いかにして未来に対する自信を高め、企業の借り入れ意欲を刺激するかということです。自信が不足している状態では、企業は借り入れをしようと思わなくなりますし、金利がゼロ近くまで下がっても、やはり借り入れは選択肢から外れます。これがいわゆる「流動性の罠」です。利下げは景気刺激策の一手段ですが、やるなら早いうちにやるべきだったのであり、いまからでは遅きに失した感があります。「空腹時に栄養を強化してこそ、その効果が鮮明に現れる」というわけなのです。

いくつもの要因が重なり、経済の下振れを招いている状況では、通貨政策の伝達作用は間違いなく弱まり、「流動性の罠」に陥る可能性すらあります。経済が下振れしているときは、通貨政策の効果は限定的であるため、財政政策と平行して実施するのではなく、付帯条件として位置づけるべきなのです。例えば、中央政府が国債を発行した際、通貨政策はこれに協力する施策として、二級市場あるいは一級市場で国債を買い付けます。公開市場操作では、国債という選択肢を多めに用いて中国人民銀行のバランスシートにおける中国債の割合を高めるべきであり、これまでのように機械的に「中央銀行の独立性」を強調するだけではいけません。財政・通貨政策が一体化した新たな協同枠組みを構築し、国家ガバナンスという高みから2大政策がタッグを組んだパワーを発揮できるようにしなければなりません。

「マクロコントロールの意思決定と執行を完全に中央に戻すべき」

記者:現行のマクロコントロールモデルの深部には、どういった問題が存在するのでしょう。また、どのように刷新を進めていくべきでしょうか。

劉尚希:中央と地方との関係は、国家ガバナンスに属する問題で、マクロコントロールに直接反映されます。2008年以前のマクロコントロールは、中央主体でおこなっていましたが、現在は地方主体になっており、「中央によるコントロールの地方化」が起きています。

1998年にアジア金融危機が発生した当時も一連のマクロコントロールがおこなわれました。このときは、中央が長期建設国債を発行し、その資金を地方に貸し付ける方式が採られ、地方が各種の投・融資プラットフォームを通じて借り入れや財政拡張をすることは制限されていましたし、地方が債券を発行することや財政赤字を出すことは禁じられていました。しかし2008年のリーマンショック対策として打ち出された「4兆元の景気刺激策」では、中央が1.18兆元を調達した残りは、地方に委ねられました。これを機に地方は、投・融資プラットフォームを頼りに融資を募り、積極的な財政拡張に乗り出すようになり、大量の債務が発生していまに至っているわけです。いまはさらに不動産市場の景気悪化により、地方の土地譲渡収入は大幅に減少しています。

以上のような経緯で2008年を転換点とする変化が生じたわけですが、このようなマクロコントロールモデルの効果はどんどん薄れ、持続が難しくなっています。地方への投資は現在のところ、中央がランク付けする特別債の指標が唯一の基準になっています。しかも地方の財政難が叫ばれる中、これ以上拡張する余力もなく、地方によっては、拡張どころか収縮しているところもあります。それゆえ、経済復興を実現するためには積極的な財政政策の実施が必要ではあるものの、再び地方財政に頼ろうとするなら、それは無理な注文というものです。「中央によるコントロールの地方化」メカニズムの下で積極的な財政政策を強化しても、実際の効果はあまり得られないでしょう。

また、中央政府は現在、地方の債務拡張を厳しく制限しており、レバレッジをかけることはできません。そのような状況下で、債務リスクを考慮し、地方にレバレッジを引き下げるよう要求する反面、積極的な財政政策の面からは地方にレバレッジの強化を求めるというのでは、地方は対応に苦慮してしまいます。したがって、積極的な財政政策を実施するには、中央政府が主体となって景気のてこ入れをするべきであり、こうすることでマクロコントロールにおける板挟み問題も一刀両断に解決できます。

ですが実は方法があります。それは、まだ余裕のある中央が主体となってレバレッジをかけることです。目下のところ、GDPに占める国債の割合は高くありません。中国の地方債の発行額はいまや国債を上回っており、こうした地方に頼ったマクロコントロールモデルは効果が薄れる反面、リスクは上昇しています。ここらで原点回帰し、マクロコントロールの意思決定と執行を完全に中央に戻すべきです。

記者:目下の地方財政には、地方債の残高が多すぎること、利息負担が重くのしかかっていること以外にも、経済復興に影響を与えるような突出した問題があるのでしょうか。

劉尚希:まずは地方債をこれ以上拡大しないことが必要です。これ以上増発してもあまり効果は望めません。しかも、地方では条件に適合するプロジェクトがそれほど多くないにも関わらず、省が債券を発行して資金を調達し、それを市や県に分配して相応のプロジェクトを探させるなど、プロジェクト投資自体がどんどん下級の自治体に移行しています。市や県は規模が小さいため、投資プロジェクトを見つけること自体が難しいです。いまは地域経済の二極化が顕著になっていて、県レベルでは多くのところで人口流出が続いています。そんな場所で条件に合うプロジェクトがいくつ見つかるというのでしょう。

また、大きな流れで言えば、人口の都市化〔農村戸籍を都市戸籍に変更する政策のこと〕をさらに進め、「逆都市化」を防止し、空間的に都市群や中心都市を取り囲むような形で投資プロジェクトを配置することが大切です。単に資金を下へ下へと分配し、市や県、ひいては郷・鎮にプロジェクト申請をさせるようではいけません。いまは特別債の資金をプロジェクトに支給する際、地方が上級の自治体に申請するという形を取っていますが、これは問題です。簡単に市や県にプロジェクト申請をさせるべきではなく、申請してきたとしても参考に留めておき、経済の地域一体化や、現下の人口流動、産業集積に基づき、省レベルで一括して投資プロジェクトを手配しなければ、真の効果は得られません。省が一括手配することで、たとえ短期的な経済効果は得られなくても、社会的効果は得られます。いまは社会的効果すら見えない投資プロジェクトが多いです。原因は人口減少です。プロジェクト投資において、人口動態とプロジェクト分布の矛盾が生じると、投資効果はどんどん薄れていきます。

さらに言えば、特別債の設定当初の構想に調整を加え、現状に合わせて最適化することも必要でしょう。マクロ的に見れば、地方特別債はこれ以上発行すべきでなく、残り枠を国債に回し、中央政府のほうでレバレッジを実行するべきです。社会インフラ建設プロジェクトは経済および社会の主体となる空間を対象とし、県や郷から市以上の自治体へ移行すべきで、人口流出が続き、潜在成長力の小さい地方は、プロジェクト配置を減らしていく方向にしなければなりません。

民間企業によく効く「精神安定剤」を与え、自信回復を図るべき

記者:いま、経済を立て直すためには、早急に不動産政策を改正して不動産市場を救うことから着手すべきという意見が多いですが、先生はどうお考えですか。

劉尚希:いまの不動産市場には多角的アプローチが必要です。不動産業界はモデルチェンジが必要ですが、だからと言って単に旧路線に回帰するだけでは、いま以上に深刻な問題が生じるでしょう。現在、一・二線都市の低所得者層は住宅を購入することができずにいますが、彼らの居住権を保障するため、公営住宅や長期賃貸住宅などの賃貸住宅市場を大々的に発展させるべきです。

不動産業を発展させるためには住宅を売れという考え方はもう古く、これからは賃貸住宅の建設を奨励し、政府から補助金を受けたり政府に買い取ってもらう方式にすべきです。低所得者層のそれぞれの所得水準に合わせた賃借料体系と退去メカニズムを確立し、商業モデルとして持続可能な運営を目指します。いくつかの地方を視察に訪れてみましたが、賃借料が安すぎたり、公営住宅が払い下げられたりしていました。そうなると大量の財政補助が必要になり、賃貸住宅の供給はどんどん先細りになっていきます。

そうならないためには、公営住宅や長期賃貸住宅などの賃貸住宅市場を大々的に発展させ、低所得者層の居住ニーズを保障する一方で、制限措置を撤廃し、高級分譲住宅は市場の調節メカニズムに完全に委ね、硬直的需要者層を分類・分析し、地価や土地供給などの面から計画的に手配することが必要で、一律の対応をしていてはだめです。政府の役割と市場の役割をそれぞれ発揮し、両者の力が結びついてこそ、「房住不炒」は実現できるのです。単に不動産市場を開放し、購買欲を煽って住宅を購入させるだけでは元の木阿弥に戻ってしまい、いずれまた立ち行かなくなります。

2022年4月17日、四川省成都市初の保障性賃貸住宅〔政府による補助がある低中所得者用賃貸住宅〕プロジェクトで分配が始まった。写真/視覚中国

記者:市場は投資を促進し、需要を刺激する一連の政策に期待が高まっていますが、いま政策が注力するのはどういった点だと思われますか。

劉尚希:現状を考えると、一貫性のない監督管理政策をまずは改め、アウトな行為を明確に示し、民間企業によく効く「安定剤」を投与する必要があるでしょう。既存の「安定剤」ではもう不十分だと思われます。知的財産権の保護や公平な競争の審査などの面では、通り一遍の対応ではなく、本気の対応を示す必要があります。これは景況感を安定させ、自信を高めるために非常に重要なことです。

次に、中央政府による景気のてこ入れも大変重要です。農民工の市民化に関して重点的に手を打ち、都市群や都市圈を囲むように投資プロジェクトを配置します。市場にできることは市場に任せ、政府は市場による投資を締め出さず、社会による投資を牽引し、市場が望まないまたはできないプロジェクトに注力すべきです。農業移動人口の市民化に関連する投資は膨大な成長の余地があり、当面の投資や内需を拡大できるだけでなく、農民の市民化を進め、農村振興を牽引することも可能です。

3つ目に、デジタルプラットフォームなどの大手企業に対し、就業問題の解決や中小企業の発展において力を発揮させることが必要です。中小企業の発展はこれら大企業なしにはあり得ず、製造業などでは数多くの中小企業が大企業の下請けを担っています。大手企業が生き残ってこそ、下にいる者も生き残れるのです。大企業に自信がみなぎり、投資を拡大するようになれば、多くの中小零細企業の拡張も自ずと促されます。大・中小・零細企業を1つの有機体として捉えることが大切で、単に社会の就業安定のために中小企業の支援をするという態度ではいけません。産業ピラミッドの安定は、これら大手企業が頂点に君臨していてこそ保たれるわけであり、そのポジションに穴が開けば、産業ピラミッドの安定は保障されません。

5月4日、山東省青島市のある民間輸出企業の生産工場。写真/IC

以上は応急的対策ですが、それとは別に抜本的対策も講じる必要があります。抜本的対策というのは、即ち構造改革のことで、都市と農村という二元構造を取り払い、人を中心とした都市化を推進するのです。最近の研究によれば、都市の人口増加と消費・需要の拡大とは正比例の関係にあるそうです。都市の人口が拡大を続けてこそ、内需も成長を続けられるのです。また別の研究によれば、農民が農民工になることで、消費は30%拡大し、農民工が市民になることで、消費はさらに30%拡大するそうです。ここからも、都市の人口増加と消費・需要の拡大およびアップグレードは、密接に比例していることが分かります。

都市と農村という二元構造は、経済の二元構造だけでなく、社会の二元構造をももたらしました。農民の市民化を進め、相応の公共サービスを提供する方法を早急に考えなければなりません。例えば、農民が都市に移住する際に住宅保障をするなどの政策により、不動産業のモデルチェンジを図ることができます。人口流動に基づく公共サービス投資および公共サービスインフラの建設を大々的に拡大し、この分野から経済活性化を図っていくべきでしょう。そのためには、空間形態から問題を考察し、都市圈や都市群に対策を講じるべきです。基本的な公共サービスを均等化するには、地域の固定した「右へならえ」という慣習を打破し、特に大都市が率先して、農民工の住宅、医療、子女の教育などの面で改革を断行し、都市の住民と同様の待遇を受けられるようにしなければなりません。都市は緑化・低炭素化だけでなく、包容力を備えることが、社会および経済の活性化において非常に有利に働くのです。

※本稿は『月刊中国ニュース』2023年10月号(Vol.138)より転載したものである。

https://www.jnpc.or.jp/archive/conferences/34806/report

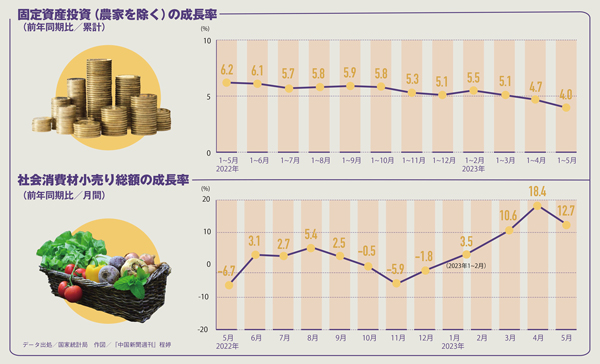

今年の中国経済成長率に底打ちの兆し

濱本 良一 (読売新聞出身・国際教養大学教授)

日頃、中国経済を強く意識させられるのは、一挙手一投足に敏感に反応する日本の株式市場ではないだろうか。一方、論壇では「中国経済崩壊」といった極論が飛び出す。大きくぶれる背景には情報の公開性=透明性の欠如がある。

その意味では、中国財政省や国務院(内閣)直属シンクタンクから派遣されたエコノミスト5人が、経済分野の現状を報告した会見は中国側の努力として評価されるべきだろう。ちなみに同様の会見は昨年9月に続いて2回目である。

2016年の経済成長率は6.7%増だった。過去40年近い改革・開放での3大ピーク値15.2%(1984年)、14.2%(1992、2007年)と比べると半分以下で、過去6年間、連続して下降線を描き続けている。しかし、畢吉耀氏は「今年は景気の下振れ圧力が軽減し、1~2月の工業生産高や発電量、消費インフラや不動産への投資がプラスで、今年第1・四半期の成長率は昨年の6.7%を上回る見通しだ」と述べた。通年でも下げ止まる兆しなのかもしれない。

劉尚希氏は、投資主導から減税・企業の負担軽減へと変化する財政政策を紹介し、雇用・教育・介護・年金の充実など社会政策にも重点を置いていると強調した。

趙晋平氏は、3月17日に国連安保理で採択されたアフガニスタン問題決議で、「一帯一路」構想が地域経済協力を推進するものとして取り上げられたことを明らかにした。

日米両国が参加を見合わせるアジアインフラ投資銀行(AIIB)の加盟メンバーは70カ国・地域に上り、アジア開発銀行(ADB)の67カ国・地域を上回った。周強武団長は「18年末で拡大手続きが終了するが、あと20カ国・地域が加盟申請中だ。最終的には世界最大の地域開発機関になる」と自信を示した。

質疑応答では、トランプ米政権の保護主義に対する率直な発言が印象的だった。樊綱氏は「人民元は、ドルとともに上昇し、過度な元安にならないようにしている。米国が中国を為替操作国と認定することはできない」と断定した。趙氏は「トランプ氏は選挙戦中に一帯一路構想に注目し、興味があると述べていた。AIIBや同構想に関して、中米両国はインフラ問題で話し合うし、協力に向けた大きなチャンスがある」と期待感を表明した。

米国がTPP(環太平洋経済連携協定)離脱を表明した点に関し、趙氏は「TPPが高度な貿易・経済ルール作りを目指したので中国は参加しなかったが、オープンな態度に変わりはない。発効を願っている。われわれは交渉期限が年末に迫った東アジア地域包括的経済連携(RCEP)交渉の妥結に向け、グローバル化と地域経済一体化促進のため貢献していきたい」と述べた。中国とともにRCEPに加盟する日本の役割が一段と求められよう。

2017

https://youtu.be/8O2RYcNyQrI?si=QRB4f7izsFhYyQzq

劉尚希 / LIU Shangxi

中国 / China

財政部財政科学研究院院長

2016

https://youtu.be/y_mVDevA2Fs?si=tN4-uPuKbDPIjdoN

https://www.bloomberg.co.jp/news/articles/2023-07-13/RXQ0ROT0AFB401?utm_source=twitter&cmpid%3D=socialflow-twitter-japan&utm_campaign=socialflow-organic&utm_medium=social&utm_content=japan

景気減速で決定的措置迫られる中国、考え得る6つの選択肢

A Chinese flag in front of buildings in Pudong's Lujiazui Financial District in Shanghai.

Photographer: Qilai Shen/Bloomberg中国は政府借り入れを増やし、企業への税制優遇措置を拡大するとともに金利を引き下げ、経済を活性化させ失業率の上昇を抑えるべきだ。

これらは政府に関係するエコノミスト数人と尊敬される元政策担当者の見解で、景気減速に対応するため決定的な措置をとる緊急性は増しているとの見方を全員が示した。

Weakening Recovery

China's growth seen losing steam in 2Q after rebound in early 2023

Source: China's National Bureau of Statistics, Bloomberg

Note: Second-quarter y/y projection compares with a period in 2022 characterized by lockdowns and Covid restrictions, and so has a low base of comparison.

中国経済には警戒すべき兆しが見られている。不動産市場のきしみは大きくなり、インフラ投資は頭打ち、輸出は縮小している。若者の失業率は過去最高で、デフレリスクが近づきつつある。こうしたあらゆる問題が、企業と消費者の信頼感を圧迫する。

景気を再び回復軌道に戻すため、政府がとり得る選択肢には以下のようなものがある。

政府借り入れの増額

中国政府は3月に3兆8800億元(約75兆円、地方政府に発行が認められた特別債の額を除く)に設定された今年度財政赤字を拡大することが可能だ。だが、政府は二の足を踏むかもしれない。2008年の後に見られたように、赤字急増に伴う長期的なリスクが発生するからだ。

それでも短期的な財政出動は経済をなお支えることができ、迅速に行動すればコストを比較的低く抑えることができると、楼継偉元財政相は主張する。

楼氏は国務院系の新聞、経済日報が9日の一面に掲載した記事で、「できるだけ早く経済を通常の状態に戻すため、可及的速やかに財政赤字を拡大させるべきだ」と論じた。

Broad Budget Deficit

China's fiscal gap much bigger when special bond sales are included

Sources: China's Ministry of Finance reports

Note: Figures for 2023 are budget forecasts.

楼氏は今年の財政赤字を最大2兆元増やすよう政府に求めた。公式データに基づきブルームバーグが試算したところでは、この増額が実施されれば財政赤字は国内総生産(GDP)比4.6%まで上昇することになる。中国政府の目標は同3%だ。

政府はまた、資金難で高リスクの地域が隠れ債務の返済資金に充てるため地方債の追加発行を認める計画を検討していると、ブルームバーグは事情に詳しい関係者の情報として今月報じた。

中央政府債

新規債務の大半は中央政府の債券発行で賄い、中小企業支援に活用されるべきだと楼氏は提唱。この資金の一部は地方に分配し、資金難の地方政府が市民に過剰な罰金を科すなど極端な動きに出るのを防ぐこともできると述べた。

中国財政科学研究院の劉尚希院長は、地方政府に比べて中央政府はなお借り入れを増やす余地があると示唆。劉氏は政府紙、中国新聞週刊とのインタビューで、人民銀行(中央銀行)は独立性を保つという「教条的な」主張を捨て、経済成長を促進する目的で中央政府債の直接購入を開始するべきだと論じた。

人民銀は長きにわたり、政府債の直接購入を求める声に抵抗している。

金利引き下げ

人民銀行は利下げを継続することで資金調達コストを低く維持し、新規債務で政府が背負う負担を緩和することもできる。銀行システムに対して流動性を追加注入すれば、増発する債券の吸収に役立つ。

China Has Been Sparing With Rate Cuts

The PBOC trimmed policy rates once this year so far

Source: The People's Bank of China

ブルームバーグのエコノミスト調査によると、人民銀行は年内の残り期間を通じて政策金利を緩やかに引き下げる公算が大きい。だが、中国の政策アドバイザーや政府系エコノミストの一部は、大幅な利下げを最近示唆し始めた。

習近平国家主席を含む最高幹部に政策を助言した経験を持つ著名エコノミスト、劉元春氏は、人民銀が金利を1ポイント引き下げれば中国全体で節約できる資金調達コストは3兆1000億元に及び、この額は今年1-5月の鉱工業企業の合計利益よりも大きいと指摘した。

人民銀の元貨幣政策委員、余永定氏は今月、利下げが「極めて必要」で、その余地は「かなり大きい」と述べた。

預金準備率

大幅な利下げよりも、はるかに可能性が高いのが市中銀行の預金準備率引き下げだ。人民銀が預金準備率を最後に引き下げたのは3月だが、中期貸出制度(MLF)の融資の返済期限を次々と迎える今年下期に流動性の逼迫(ひっぱく)を防ぐため、再度引き下げざるを得なくなるかもしれない。

Cutting Reserve Ratios

The PBOC last reduced the required reserve ratio for most banks in March

Source: People's Bank of China

経済全体の信用の伸びが弱いことを踏まえ、人民銀が市中銀行に融資を増やすよう促す可能性もある。次期総裁就任が有力視される人民銀の潘功勝・新共産党委員会書記は6月、信用の伸びが上向く余地はあると発言していた。

税制優遇

米中貿易戦争と新型コロナウイルスのパンデミック(世界的大流行)の影響を企業が乗り切るのを後押しするため、李克強前首相は大型減税の導入を指揮した。この減税規模は大きく、GDPに対する税収額は2018年の17%から、昨年は14%近くに低下した。

不動産市場が冷え込み、政府の主な収入源である土地売却収入が落ち込むなど歳入が縮小している中では、さらなる大幅減税の余地は小さいように見える。

代わって政府が注目すべきなのは既存の税制優遇措置の有効性を改善することだと、粤開証券の羅志恒チーフエコノミストが人民銀行系の雑誌「中国金融」への寄稿で指摘した。羅氏は先週、李強首相主宰の会議に出席したが、この会議で首相は、政府は「時間を浪費することなく」的を絞った景気刺激策を実施していくと述べていた。

現金給付

羅氏はまた、政府が消費者にクーポン券や現金を給付し、家計消費を支援することも提案。貧しい地域の財政負担を軽くするようコストを中央政府と地方政府で分担することも可能だと、中国金融への寄稿記事で論じた。

だが、これは可能性が低いかもしれない。パンデミック期に日本や米国などでは実施されたが、中国は消費者への大規模な現金給付を控え、雇用市場の回復が消費者の支出増加につながることに賭けた。ただ、景気の厳しさはいまだ和らがず、限定的な刺激策はこの改善にほとんど寄与していない。

関連記事

原題:Here Are the Options China Still Has for Stimulating Its Economy(抜粋)

| ||||||||||||||||||||||||

https://x.com/tetsu0724d/status/1682743078929727488?s=61

経済成長を促進する目的で中央政府債の直接購入を開始するべきとした。

人民銀は長きにわたり、政府債の直接購入を求める声に抵抗している。

金利引き下げ

人民銀行は利下げを継続することで資金調達コストを低く維持し、新規債務で政府が背負う負担を緩和できる。

銀行システムに対して流動性を追加注入すれば、増発する債券の吸収に役立つ。

人民銀行は年内の残り期間を通じて政策金利を緩やかに引き下げる公算が大きい。

だが、中国の政策アドバイザーや政府系エコノミストの一部は、大幅な利下げを最近示唆し始めた。

著名エコノミスト、劉氏は、人民銀が金利を1ポイント引き下げれば中国全体で節約できる資金調達コストは3兆1000億元に及び、この額は今年1-5月の鉱工業企業の合計利益よりも大きいと指摘。

人民銀の元貨幣政策委員、余氏は今月、利下げが「極めて必要」で、その余地は「かなり大きい」とした。

| ||||||||||||||||||||||||

https://x.com/tetsu0724d/status/1682743806180093953?s=61

ーー

0 件のコメント:

コメントを投稿